Mortgages with differentiated payments are rare these days. Because banks are more profitable when the borrower repays the loan consistently. Differentiated payments allow the client to independently choose the installment amount and even pay off the loan ahead of schedule to save money. Banks give mortgages at a low interest rate, but try to make a profit from it. Therefore, early return is not profitable for them. But if you are taking out a mortgage for the first time, then you need to understand in detail which payment schemes are more profitable and which are simpler.

Difference between differentiated and annuity payments

When drawing up a mortgage agreement, the bank offers the client a choice of debt repayment scheme - annuity or differentiated.

A differentiated mortgage payment involves paying the loan itself in the first months. Interest will be accrued monthly depending on the balance of the debt. Therefore, when the loan body is repaid, the borrower will only have to pay the interest.

For people with low earnings, this scheme does not bring benefits, since the point is to quickly repay the loan amount. Differentiated payments allow you to save on interest, especially if you pay off most of the debt during the first months.

An annuity payment is easier to calculate, because here the bank initially charges interest on the entire amount of the debt relative to the term and withdraws a monthly amount for repayment. Interest is paid first, and only after that the money is used to pay off the debt itself. Interest accrues with a certain regularity, depending on which bank you took out the mortgage from. Therefore, the schemes may vary slightly in terms of conditions.

An annuity payment is not beneficial for a person who proposes early repayment, because he will already pay all the interest to the bank.

Advantages and disadvantages of mortgages with differentiated payments

A mortgage loan with graduated payments is quite complicated when you first get acquainted with it. But if you delve into the essence of the issue, you can highlight the advantages and disadvantages of the scheme.

Advantages and disadvantages

Monthly payments are transparent, without hidden fees.

Loans with early repayment under this scheme allow you to save on interest.

When the insurance policy is renewed annually, its cost decreases.

The payment amount decreases monthly and payments towards the end of the term become minimal.

Savings when restructuring a loan.

It is difficult to plan expenses due to the heavy financial burden in the first months of debt repayment.

If your financial situation sharply deteriorates, there is a risk of late payments and overpaying fines for this.

The bank is more demanding of borrowers, especially in checking financial condition and stability due to large amounts of monthly payments.

Often the loan amount is very limited.

Regular checks of the amount paid according to the payment calendar.

You need to calculate your strengths and weigh all the pros and cons of a differentiated repayment scheme before applying for a mortgage. If the choice is made, then you need to find out which banks provide mortgages with differentiated payments.

What is the essence of differentiated payments?

When applying to banks for a mortgage, the borrower, as a rule, first of all takes into account the interest rate. Much less often, he studies the terms of the loan program for the presence of various types of commissions. But almost no one pays attention to the payment system. However, you should know that the final cost of the loan depends very significantly on the method of repayment specified in the agreement.

A differentiated mortgage provides for the payment of the principal portion of the debt in equal installments, while interest accrues on the balance of the loan. It follows that the amount of interest gradually decreases.

As a result, the monthly payment amounts will differ. The borrower must be prepared for the fact that in the first years, payments on a loan with differentiated payments will be especially noticeable, but over time it will become easier to repay the loan.

This factor serves as an additional reason to carefully check the financial status of a potential client. Bank specialists will predict the possibility of making large payments in the initial lending period. Moreover, to reduce the risk of non-repayment, such a calculation is made using safety coefficients, which, of course, reduces the chances of receiving a loan.

Like any banking product, a mortgage with differentiated payments has its advantages and disadvantages.

pros

The advantages of this type of loan include:

- Significant savings when repaying early: no interest is paid on the remaining balance.

- The payment structure is clear and simple.

- The cost of insurance is lower because the loan amount decreases every month.

Minuses

Among the negative aspects of such a loan, experts highlight the following circumstances:

- To get a differentiated mortgage, you must have a high legal income.

- The above factor may result in a reduction in the maximum loan amount. After all, according to the law, the amount of payments should not be more than 50% of the borrower’s monthly income.

Banks that issue mortgages with differentiated payments in 2020

If you want to take out a mortgage from Sberbank, VTB, Alfa-Bank, Unicredit Bank and others, you will be faced with a lot of mortgage products, but with an annuity repayment scheme. Even the largest bank in Russia, Sberbank, prefers to give mortgages with stable debt repayment, it is more profitable. But if you are aiming to take out a home loan with a differentiated debt repayment scheme, then look at the list of banks from the table below.

| Bank | The name of the program | Credit. limit, rub. | Interest rate | Term | An initial fee |

| Rosselkhozbank | Mortgage housing lending | 100,000 – 60 million | 8.85% — 12.0% | Up to 30 years old | More than 15% |

| Mortgage under two documents | 100,000 – 8 million | 9.35% | Up to 25 years | More than 40% | |

| Gazprombank | Primary market | From 500,000 | From 9.2% | Up to 30 years old | More than 10% |

| Secondary market | From 500,000 | From 9.0% | Up to 30 years old | More than 10% |

These two banks offer the best mortgage terms for 2020. Banks take into account the wishes of clients regarding the payment scheme. The decision to assign a method of debt repayment is made after reviewing the client’s application, checking the credit history and financial condition. Review information on official websites and select a lender.

Mortgage according to a differentiated scheme

The following credit institutions offer this mortgage repayment option:

- Rosselkhozbank. At the beginning of 2020, 7 mortgage offers are relevant, the terms of which can be studied on the official website. Before completing the application, it is proposed to make a preliminary calculation in the loan calculator, where the choice of the option of annuity or differentiated payment is active.

- In 2020, Gazprombank offered various mortgage programs for borrowers. They are also relevant this year. By filling out the form on the website, you can receive a preliminary payment schedule. More information about products is provided by employees at bank offices.

Look at the same topic: Mortgage for a family with 2 children in [y] year: conditions, state support for mortgages

The differentiated mortgage contribution for 2020 is not presented in the offers of all banks. The trend continues in 2020. The reason for this limitation is explained by the lender's interest in obtaining the maximum benefit, given that the interest rate is gradually decreasing.

Calculator to calculate benefits

It is almost impossible to refinance a mortgage loan, take a vacation, or ask for restructuring. Therefore, it is necessary to calculate the overpayment on the loan before submitting the application. Using a mortgage calculator, interest rates can be calculated within a minute. You need to fill in the empty columns with the loan parameters and immediately get the result. A preliminary calculation using a mortgage calculator will help you navigate the benefits of each method of debt repayment and calculate comfortable terms.

Annuity and differentiated payment - what is it and how to calculate it?

When applying for a mortgage loan, the bank asks the borrower to select loan parameters.

They largely depend on the chosen debt repayment scheme. The loan is repaid in monthly payments - this is the only established banking system. The borrower needs to return the loan amount and the interest accrued on it. You can pay the amount in equal parts - an annuity, or deposit money in different amounts - differentiated payments.

Annuity payment

The annuity scheme involves making equal monthly contributions. The bank sets the amount of the regular payment depending on the size of the loan and the chosen term. Interest is immediately charged on the entire loan, and the bank divides the amount of interest and loan by the number of months. The amount is calculated using a special algorithm and the employee announces the amount of the monthly payment to the client before concluding the contract.

An annuity payment is convenient, but making early repayments with it is pointless; the savings will be minimal. The annuity scheme is designed to pay mostly interest at first and less of the loan body, but by the end of the term everything changes. Because of this, when asked to recalculate the loan amount, it turns out that all interest has already been repaid, and the bank cannot reduce the amount of the loan itself.

Each of the schemes has its own characteristics, but it is difficult to find the second one in the banking market.

Differentiated payment

In an alternative method of repaying a mortgage loan, the bank calculates the amount of the monthly installment depending on the balance of the debt. Every month the amount of interest decreases and it is easier to pay the loan. But initially the client will have to deposit large amounts, where the interest part is significantly less than the loan amount.

With a differentiated payment upon early repayment, the borrower can save, since the amount of interest is calculated from the balance of the debt, and it has already been repaid to a greater extent. But you need to find out not only which banks provide mortgages with differentiated payments, but also what are the conditions for calculating the amounts.

Due to the financial burden on the client in the first months of the mortgage, a loan with differentiated payments is not approved for everyone. Only borrowers with high official income can count on it. Since, according to the law, the payment amount should not exceed 50% of the monthly salary.

What are differentiated payments

Any loan with any repayment system consists of two parts:

- loan body - the amount received by the borrower;

- interest on the loan.

Differentiated payments is a loan repayment system in which the borrower pays the principal portion of the debt in equal installments, and interest is charged on the unpaid portion of the loan.

The difference between annuity and differentiated payments is how interest is paid:

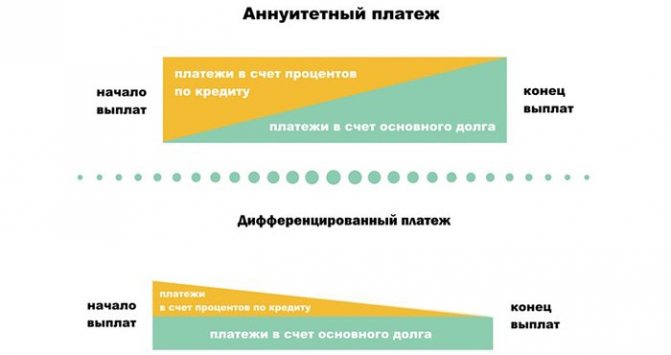

- In the case of annuity payments, interest on the loan is paid unevenly: in the first payments, most of the interest is taken up, and the loan body takes up a smaller part. Therefore, by the middle of the loan repayment period, the borrower repays significantly less than half of the loan itself. However, the monthly payment does not change from the beginning until the mortgage is paid off. In case of early repayment of annuity payments, the entire overpayment goes to the principal amount of the loan;

- The payment structure under the differentiated method is simpler: the loan body is repaid in equal parts, and the amount of interest gradually decreases, since they are accrued on the balance of the debt - and it is gradually reduced. As a result, the monthly payment will be different every month. In the early years, the borrower bears a significant debt burden, but over time it becomes easier to pay the mortgage.

Due to the complex formula, calculating the annuity payment is quite difficult. It is problematic to say how the overpayment will ultimately differ on loans with the same amount but different repayment systems. But in most cases, the overpayment on a mortgage with differentiated payments will be an order of magnitude less.

Credit Guarantee Agency - support for medium and small businesses.

You will find all possible types of loan repayment in our material.

Calculation and formula of annuity payment: https://creditbery.ru/credits/ipoteka/formula-annuitetnogo-platezha.html

Is it possible to change the annuity payment to a differentiated one?

Once a mortgage agreement has been concluded, the loan repayment scheme cannot be changed. Banks give mortgages under certain conditions, and annuity is more profitable for them. But if the client wants to save money and has additional funds, then it is possible to repay the mortgage debt ahead of schedule.

There is no need to pay an early repayment fee.

To do this, you must notify the bank orally or in writing (early repayment requirements are specified in the mortgage agreement) of your intentions. Indicate the amount to be deposited and the date of the transaction. After the money is credited to the account, the amount of principal and interest will be recalculated, and the client will be given a new payment schedule. The operation can be carried out an unlimited number of times, the amount of contributions does not matter.

Be sure to notify about partial or full repayment ahead of schedule to avoid confusion and banking errors.

Features of two payment options

The list of credit institutions operating under the differentiated loan payment scheme is constantly shrinking. Annuity contributions bring great benefits to banks and the opportunity to earn a profit in the form of interest in the first years of loan repayment. If with a differentiated scheme the payment is gradually reduced, then with annuity payments the value is always constant, both in the first year and in the last months of loan repayment.

If all payments according to the schedule are written out in two columns, principal and interest, then you will notice the following pattern:

- A differentiated contribution is the repayment of debt in different payments, which decrease every month. Consists of a share of the principal debt and interest on the balance. The debt payment is always the same. Interest payments decrease every month.

- The annuity payment is always constant, but most of the payment amount is spent on interest and only a minimal amount of money is spent on repaying the debt. The excess of loan repayment over interest occurs only in the second half of the entire loan period. If the mortgage is issued for 10 years, then in the first five years the bank receives its dividends and partially writes off the debt. Early repayment is not always beneficial to the client. In the first years, the amount of debt changes slightly.

The differentiated mortgage payment scheme is transparent and more profitable for the borrower. But credit institutions give preference to annuity contributions, the formation process of which is more difficult to understand, but the benefit to the bank is more significant.

Sometimes the benefits of the annuity schedule are also seen by consumers whose income does not allow them to make maximum payments in the first months, as provided for with differentiated contributions. The bank has the right to refuse or reduce the amount if there are doubts about the financial capabilities of the applicant.

The annuity payment is usually less than the differentiated one if we are talking about the same lending conditions (amount, repayment period and annual interest). This increases the chances of your application being approved.

Look at the same topic: Mortgage for the construction of a residential building in Rosselkhozbank [y]

What do you need to get approved for a mortgage with differentiated payments?

It is difficult to obtain a mortgage with a differentiated payment scheme, because banks are strict with potential borrowers due to the high risk of non-repayment. A person must:

- Be officially employed. The request is submitted to clarify the total length of service for the last five years (must be more than a year) and length of service at the current place of work (from 6 months). The lender is also interested in how valuable the employee is and what his career growth is. Therefore, a request is often made to collect additional information.

- Have a high salary. Its size should be enough to pay the largest payment assigned by the bank for the mortgage. Official income is taken into account, confirmed by a 2-NDFL certificate. The bank tells you either the exact salary required to take out a mortgage or the percentage required for repayments.

To increase the chances of approval for a mortgage with differentiated payments, a person can:

- Provide collateral. It is necessary to invite an appraiser to establish the exact amount, or indicate it yourself when submitting an application. But you shouldn’t lie or exaggerate; the bank regards such actions as an attempt at fraud and automatically denies the loan.

- Invite guarantors or co-borrowers. Up to 2-3 people are allowed to bring to the bank to increase the mortgage amount or receive a differentiated scheme. Their income is taken into account.

- Provide information about your ideal credit history. You can pre-order it free of charge from BKI to ensure compliance with banking requirements. If any errors are found, they must be corrected before submitting the mortgage application.

The more documents the borrower provides in support of their financial stability and security, the greater the chance of receiving approval for a mortgage with differentiated payments.

Is there any benefit to a mortgage with graduated payments?

Finding a bank that issues a mortgage with differentiated payments is problematic. This is due to two factors.

- The first is the bank’s desire to benefit from the loan; with the annuity scheme, the profit percentage is much higher. Even if the borrower decides to close the loan early at any stage. With a differentiated scheme, the amount of overpayment is smaller due to regular recalculation of debt and interest.

- The second factor is the low income of most clients. Not every person is able to withstand the financial burden of a mortgage with large down payments. When taking a housing loan, the borrower is often required to make an initial payment, and then it is difficult to pay a lot at once. In order not to take risks, banks prefer to issue mortgages with an annuity debt repayment scheme.

But the benefit for the borrower is obvious - differentiated payments allow you to save in total. If you have the opportunity to deposit a large amount at once or plan to receive income (increase in salary, inheritance rights, etc.), then it is better to choose this option. It is also more profitable to repay the debt to the bank ahead of schedule with differentiated payments, since interest is not paid immediately, but gradually, depending on the size of the debt.

Which banks issue mortgages with differentiated payments?

Here is an almost complete list of such banks:

- Gazprombank offers several mortgage programs. Under the program “Purchase of finished housing on the secondary market,” the interest rate is set from 10.5 to 14.5% (depending on the currency and the size of the down payment), the maximum amount is 45 million rubles, the loan term is up to 30 years, the down payment is 15%. You can choose to use a system of annuity or differentiated payments;

- Surgutneftegaz Bank also provides the opportunity to choose between two mortgage repayment systems. The maximum loan amount for purchasing an apartment on the secondary market is 8 million rubles, the interest rate is from 12 to 13%, the loan term is up to 30 years, the down payment is from 15%;

- Bank Russia offers mortgages with differentiated payments only for the purchase of housing under the shared construction program. The maximum loan amount is 20 million rubles, the interest rate is 16.5 to 20%, the loan term is up to 20 years, the down payment is from 20%;

- Nordea Bank is ready to issue a mortgage in the amount of up to 1 million euros (or the equivalent in rubles or dollars) at 6.5–13.25% for a period of up to 20 years, down payment - 10%.

Finding a bank that offers borrowers the opportunity to repay their mortgage in differentiated payments can be extremely difficult. The reason is simple - it is more profitable for the bank to first receive most of the interest, and then the body of the loan, since with early repayment (and in a stable financial situation, any borrower tries to repay the mortgage ahead of schedule), the borrower saves much less on interest payments, but in any case must repay the principal part of the loan - early repayment does not relieve this obligation.

In any case, the choice of the optimal mortgage payment system depends on each specific case. Therefore, the proposals of different banks should rather be evaluated, although in general the differentiated payment scheme is more profitable for the borrower due to a gradual reduction in payments and savings in case of early repayment.