A mortgage secured by existing housing is a banking service that involves obtaining money for the purchase of real estate on the primary or secondary market, subject to the provision of existing property as security. In this case, the borrower manages the purchase, but in case of delays in payments, the bank has the right to apply to a judicial authority and, by its decision, sell the housing to compensate for the costs. The remainder of the funds is returned to the debtor. What are the features of such a service? What is stipulated in federal legislation? Which banks issue such mortgages and under what conditions? We will consider these and other nuances in the article.

Main requirement

Real estate collateral is a basic condition of a mortgage. The loaned object or other housing at the borrower’s disposal serves as collateral. In the first case, the financial institution issues a loan for up to 80% of the price, and in the second - up to 60%. This means that a mortgage with collateral on existing properties is beneficial to the credit institution. The reason is to reduce risks, because if the debt is not repaid on time, the bank takes the property, sells it and is guaranteed to cover expenses.

The borrower also receives a number of advantages - the interest rate on the mortgage is reduced, the credit history is not checked so closely, and the application procedure itself is faster (the bank requires a smaller package of papers). In addition, in the presence of such collateral, the down payment is reduced or not needed at all, and the term of the loan varies in a wide range - from 5 to 25 years.

An important advantage is the ability for the borrower to independently select real estate. There are two transaction options available:

- Classic - payment of debt within a specified period.

- Accelerated - sale of old housing and compensation of most of the debt.

The disadvantages are the need to obtain permission (consent) from the spouse to pledge real estate with a mortgage, restriction of the rights of the homeowner and the imposition of penalties for late payments. In addition, if the debt is not repaid on time, the risk of losing the property is high.

What is specified in federal legislation?

In Russia, the Federal Law on mortgages appeared 20 years ago (in 1998). Over the years, the law has changed many times, and in 2020 it consists of about 14 chapters. They include basic concepts about mortgages and the terms of such agreements. Thus, Federal Law No. 102 states several rules that every person should know when applying for this type of loan. The property that acts as collateral under loan agreements can be real estate (must be officially registered in the Unified State Register).

It is prohibited to use individual components of housing, for example, rooms. The exception is cases when a client of a financial institution has registered such objects in advance, and they have received the status of independent real estate.

The functions of collateral cannot be performed by housing that is not subject to privatization. The Federal Law also states that the apartment remains in the possession of the borrower for the duration of the loan repayment. You can learn about other nuances of applying for a mortgage from Federal Law No. 102 of 2020.

Conditions in different banks

Each company will offer you different conditions. All programs are intended for different categories of citizens, so the choice must be approached with full responsibility.

Sberbank

This bank is ranked first among government-owned, licensed and accredited financial services organizations. It is beneficial to cooperate with both active users and new clients. The bank operates on a state basis, offers many subsidized programs, does not engage in fraud, and has extensive experience in cooperation with reliable partners.

Sberbank conditions for a mortgage secured by real estate:

- The loan repayment period is up to 20 years.

- The smallest amount acceptable for issuance is 500 thousand rubles.

- The largest amount that a client can receive is 10 million rubles.

- Sberbank has a reduction rate in the actual market price of collateral in the range of 40-60 percent.

- Mortgages are issued against apartments, plots of land, private houses, and garages.

- The interest rate starts from 14%. But, if he writes a refusal to provide services to the insurance company, then the rate will rise to 15%, that is, it will increase by 1%.

Look at the same topic: Mortgage lending at Promsvyazbank [y] - programs, conditions, interest rate, calculator and reviews

Advantages of obtaining a mortgage at Sberbank:

- A reliable, time-tested partner who goes the extra mile for its borrowers.

- Possibility of obtaining pawnshop mortgage lending, when you can leave almost any type of property as collateral.

- Salary clients receive reduced rates and benefits when processing documents.

Flaws:

- The company has unfavorable discount rates. You will be able to get a loan equal to only 40% of the appraised value of your home.

- Relatively high percentages in the absence of positive characteristics.

- Individual entrepreneurs and owners of their own businesses are prohibited from applying for the appropriate mortgage program.

Rosselkhozbank

The company offers comfortable conditions for purchasing real estate with a mortgage for citizens who want to pledge property as collateral.

The following conditions apply:

- The loan can be repaid within 30 years;

- You can only apply for a targeted loan;

- The total loan amount cannot be less than 500,000 rubles;

- The coefficient of reduction in property value is 70%;

- The interest rate can start from 11.5%, but this condition applies only to preferential, salary clients, who guarantee an increased level of reliability.

Advantages:

- The main advantage is considered to be the excellent discount rate. You can get up to 70% of the price of your apartment on credit.

- Average interest rate.

- Profitable terms.

VTB 24

VTB24 Bank is second in the list of the best banks in Russia. Good conditions apply to clients who have proven themselves to be responsible users.

The tariff plan includes:

- Possibility to take out only non-targeted loans as collateral.

- Discount reduction factor – 50%.

- The interest rate is fixed – 11.5%.

- The loan term is no more than 20 years.

- Amount 0 to 15,000,000 rubles.

VTB24 Bank has many advantages:

- Wide coverage of the bank;

- There are many offices in every city, in almost any area;

- A good bet that won't move up.

Gazprombank

From Gazprom you can get a loan:

- For 15 years (no more);

- Up to 30% of the price of your collateral housing;

- With an interest rate of 11.75%;

- Up to 30,000,000 rubles;

- With mandatory title insurance.

Sovcombank

The company can approve different types of loans, including those collateralized by existing real estate. Security will include not only apartments and houses, but also plots of land, commercial property, garage buildings and summer cottages.

The standard interest rate will be 18.9% per annum; you can borrow up to 30,000,000 rubles. The amount cannot be more than 60% of the value of the pledged subject.

Mandatory condition: the borrower must live where he is applying for the loan (have permanent registration). You must indicate two telephone numbers in your data: landline and cell phone.

Tinkoff

The company operates remotely; you will not find a representative office of this bank in any city. All operations are carried out over the telephone or through the company’s website.

Tinkoff offers customers a credit card with a limit of up to 300 thousand rubles, which can be ordered in the application and on the website. You can arrange delivery by courier and the product will be delivered to the specified address.

You can repay the borrowed funds without interest within 55 days. About 30% of the funds spent will be returned to you as cashback. The cost of annual maintenance is 590 rubles.

This money can be used for the down payment on your mortgage. If it is not possible to return them within the specified period of time, then it is better to participate in the partnership program with Tinkoff. The manager will select a loan program for you, send you your documents and help you obtain insurance.

Alfa Bank

Mortgage lending conditions from Alfa-Bank are most beneficial to salary clients. They have a minimum interest rate of 9.75% per year.

The following programs operate with the participation of collateral:

- "Mortgage for young people."

- "Mortgage with maternity capital."

You can get from 300,000 to 1,000,000 rubles. The tariff is more suitable for those who have managed to collect a certain amount for an apartment and are ready to make a down payment.

Renaissance Credit

Here you will receive a mortgage loan at a reduced rate of 13.9 percent per year. Amount – up to 700,000 rubles.

Working with Renaissance Credit is beneficial, as the client receives:

- Convenient interest rate;

- Comfortable loan repayment conditions;

- Individual approach to everyone.

Mortgage programs secured by existing property may offer the client different rates and tariff plans. Before contacting the bank, it is necessary to analyze the further plan of action.

What are the requirements for collateral?

When issuing a loan, the bank carefully evaluates the client and the apartment that it offers as collateral. Let us highlight the main requirements for housing:

- Liquidity. Those objects that can be easily sold on the secondary market are accepted as collateral.

- Condition of the structure. When assessing, the bank pays attention to the accident rate and level of wear and tear of the building. Apartments in dilapidated buildings that are under threat of demolition will not be accepted.

- Number of owners. If one of the owners is a minor, it will not be possible to use such property to obtain a mortgage.

- Age. Financial institutions will not accept apartments that are older than fifty years.

- Layout. If the owner independently changed the layout, but did not approve it at the official level, the likelihood of receiving a loan is reduced to zero.

- Type of structure. Banks prefer real estate that is located in multi-storey buildings. If the apartment is located in a dilapidated 2-story building (including one made of wood), the property will not be accepted.

Types and conditions of banking programs

In 2020, credit institutions offer various programs to clients. The following options are popular:

- Mortgage secured by land. As in the case of an apartment, the bank checks the liquidity of the plot, evaluates it and requires the borrower to provide a complete package of papers for the property.

- Mortgage secured by a share in an apartment. This lending option is also possible, but banks are reluctant to accept it.

- Targeted (non-targeted) mortgage secured by real estate.

In general, banking services in the field of mortgage lending are divided into two categories:

- Mortgage loan to improve living conditions.

- Basic lending for the purchase of housing.

The peculiarity of the first option is the transfer of money by the bank for the purchase of real estate with the registration of a pledge. The agreement between the parties states the obligation to sell the collateral to pay off the debt (if necessary). At the same time, the period for selling housing is set by the credit institution. This transaction option, as a rule, allows you to avoid an advance payment, but the lending period is limited. In addition, the loan size is limited to 80-90% of the cost of the apartment.

Basic lending does not require the borrower to sell the property (apartment or house) that serves as collateral. All that is required is to make timely monthly payments (“body” and interest on the loan).

Which banks provide mortgages secured by real estate?

There are many interesting offers on the market, including mortgages secured by real estate. Let's look at the most profitable ones at the moment.

Sberbank

Sberbank offers several mortgage programs to choose from:

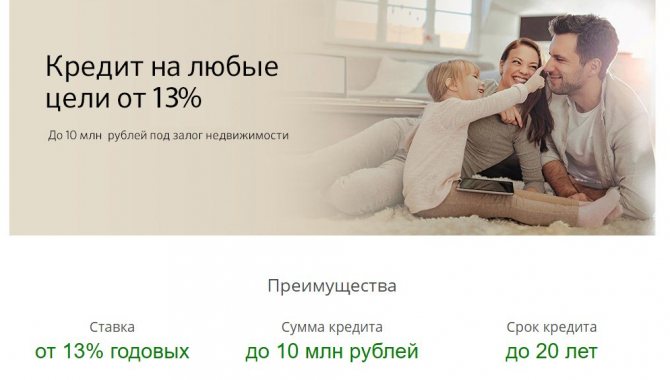

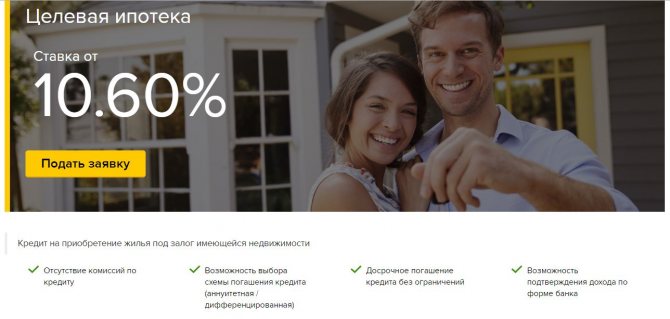

- Targeted mortgage with a down payment for finished or under construction apartments. Depending on the terms of the transaction, the interest rate ranges from 8.2% (promotion for new buildings) to 13%. Salary employees of the bank who have registered the transaction online and insured their life and health can count on a minimum interest rate on such a loan. Both purchased housing and existing real estate can be provided as collateral. The maximum loan period is on average 30 years, the loan amount to be issued is from 300,000 rubles.

- Not a targeted loan secured by existing housing. The peculiarity of such a mortgage at Sberbank is up to 10 million rubles for any purpose. If the loan amount does not exceed 60% of the market value of the mortgaged property, then for insured bank employees the rate will be 12.4%. The loan is issued for a period of up to 20 years.

VTB 24

This bank also has a loan program secured by existing housing. The main feature of such a mortgage at VTB-24 is that the mortgaged housing must be located in the city where the bank branch is located. In this case, a property can be mortgaged only if it belongs to the borrower himself or his family members. They must become guarantors.

The minimum possible interest rate is 9.7% per annum. This percentage is available to those who are insured and receive their salary on a VTB-24 card. The loan period cannot exceed 20 years. The amount of borrowed funds must be less than or equal to half the price of the housing pledged by the bank.

Rosselkhozbank

Rosselkhozbank currently has two mortgage lending programs with the condition of collateral for existing housing:

- Not a target mortgage. The amount of such a loan cannot exceed 50% of the price of the mortgaged property. For public sector employees and those who receive their salary on a bank card, the percentage is 13.2%. The rate will increase by one point if there is no personal insurance not only for the borrower, but also for co-borrowers with income.

- Target mortgage. The interest rate ranges from 9.7% to 11.4% and depends on: the availability of insurance, salary card, loan amount, type of property being pledged. Borrowed funds can be spent not only on the purchase of housing, but also on the purchase of an apartment with subsequent renovation, the acquisition of land, or the construction of a house or townhouse.

Conditions for obtaining a loan secured by the purchased property

Credit institutions put forward individual requirements for clients, but the general rules of mortgages remain unchanged:

- The loan is provided in rubles, dollars or euros.

- The period for obtaining a mortgage is up to 25-30 years.

- The borrower reaches the age of majority.

- The amount of funds provided is up to 85% of the price of the property, which is transferred in the form of collateral.

- The rate is up to 11% (if the loan is issued in foreign currency) and up to 16% when receiving a loan in rubles.

Certain requirements are also put forward for the property. In addition to those already mentioned above, the bank checks the absence of debt and encumbrances on the apartment (house), as well as the fact that basic communications have been installed, namely electricity, water and heating. As for the building where the apartment is located, it must have five floors or more, and the year of construction must be from 1950 or higher. It is important that the structure is not in disrepair.

Collateral requirements

A mortgage can be issued against a house, townhouse, or apartment. And, for example, Sberbank considers land plots and garages as collateral. At the time of applying for a loan, the property should not be pledged in favor of third parties or seized by a decision of judicial authorities, and also be recognized as unsafe or dilapidated. It should not be on the list for major repairs, demolition, or reconstruction.

The living space must be suitable for year-round use, have a separate kitchen and bathroom, as well as working plumbing equipment, windows, doors, etc. All necessary communications (electricity, water, etc.) must be connected to it.

Mortgage secured by a property under construction

In recent years, a service that involves providing a loan secured by a building under construction has been gaining popularity. Unlike lending against existing housing, the choice here is limited. The borrower chooses from several options offered by the banking institution. In addition, the interest rate increases due to the increased risks of the credit institution (when compared with other programs).

Before providing the service, the financial institution evaluates the construction stage. If the object is located at the pit level, the likelihood of receiving a loan is low. Banks are more willing to accept apartments in buildings whose construction is nearing completion. Most often, a mortgage is available when the property has passed inspection by the commission. The advantage for the borrower is that he gets a new property and saves on the price.

Maximum cost

You cannot take out a mortgage for 20,000,0000 rubles, leaving as collateral an apartment that costs 4,000,000 rubles. It will not be very profitable for the company to formalize such a transaction. The value of real estate plays an important role.

If you want to take out a loan of 5,000,000 rubles, then you need to pledge property whose price is at least 5,600,000 rubles.

Banks require that there be a slight difference in price towards the collateral. This guarantees financial security if the client:

- Will regularly be late in payments;

- Refuses to pay the loan fee;

- Due to circumstances, he will disappear from the bank’s sight, the company will lose contact with him;

- He will be unable to work.

Look at the same topic: What is a “wooden mortgage” from Sberbank? Program overview

When pledging, not only the amount plays a role; after that, the appraiser looks at:

- Level of property liquidity. They will not accept premises located on the outskirts of the city. If there is no demand for it, the bank is not interested.

- Condition of the building. The appraiser looks at the level of accidents and wear and tear.

- The house must be no older than 50 years.

- Apartments that are located in two-story buildings and are made of wood are not accepted as collateral.

- If a person under 18 years of age is entered in the “owners” column, the bank will immediately issue a refusal.

Advantages of a pawnshop mortgage

Lending against existing housing is often called “pawnshop”. Its advantages for the client are obvious:

- The interest on a loan with such collateral is lower when compared with a classic mortgage. Every year this advantage is leveled out and gradually disappears.

- Opportunity to purchase any real estate, including on the primary market. Accreditation of the structure by a credit institution is not required.

- The loan period increases to 30 years and there is a chance to pay off the debt early without the risk of fines.

- The amount of the advance payment is minimal or not at all (many banks take this step).

- Loyal requirements for the borrower and the purchased property. The main conditions are age in the range of 18 to 65 years, as well as the presence of a stable income.

Among the disadvantages, it is worth highlighting the high risk of rejection of the application when the liquidity of the property is low (this was mentioned above), high costs for obtaining insurance and the appearance of bans on the use of the apartment (for example, it will not be possible to sell it).

Is a pawnshop mortgage profitable?

The benefits of a pawnshop mortgage directly depend on the reason why you chose this particular loan. So, if a family has a good income, but they are unable to save for a down payment. They have parents who are ready to provide their apartment as collateral. For such a family, a loan secured by their parents’ home is a profitable deal.

Expert opinion

Alexander Nikolaevich Grigoriev

Mortgage expert with 10 years of experience. He is the head of the mortgage department in a large bank, with more than 500 successfully approved mortgage loans.

A non-target mortgage is advantageous in that the borrower does not need to report to the bank about the money spent. You can spend them on repairs, on purchasing a home, and even on purchasing a car. But if you have your own home and money for a down payment, then it is better to take a conventional mortgage. There you can also mortgage your existing property, but the interest rate will be lower.

A pawnshop mortgage is beneficial as a subsequent investment of your own investments. For example, when you have an apartment, but want to buy housing for the future of your children. You can get a mortgage without a down payment secured by an existing apartment, and rent out the purchased property. The rent will cover the loan payments and the housing will pay for itself without large investments on your part.

Advantages of a mortgage loan secured by real estate:

- No down payment.

- Speedy issuance of borrowed funds.

- When taking out a non-targeted mortgage, there is a smaller volume of documents to be submitted, and there is no need to confirm the intended purpose.

- When applying for a target mortgage, there is a wide range of purposes, including the possibility of purchasing a plot of land.

The intricacies of applying for a mortgage secured by existing housing - an algorithm of actions

The process of obtaining a loan to purchase an apartment is as follows:

- We choose a banking institution and a lending program. During the assessment process, attention is paid to the organization’s experience, its financial parameters, ratings and outside reviews. Additionally, the more loan programs an institution offers, the better.

- We collect the papers and submit the application to the selected bank. If you have a ready-made package of documentation on hand, the registration process goes faster. In particular, an extract from the Unified State Register, a technical passport for the pledge, papers confirming the absence of encumbrances, an assessment report, and a cadastral passport are required. In addition, the bank will require confirmation of the fact that there are no debts on utility bills. This list is approximate and often differs depending on the bank.

- We are waiting for the evaluation to complete. There are two ways available here - find an independent company with accreditation and use its services, or entrust this work to firms that work with lenders. In the second case, there is a high risk of underestimating the value of the object, and the costs are higher. It is worth considering that the assessment report is valid for up to 6 months.

- We draw up an agreement. Many borrowers make a grave mistake - they sign the agreement, but do not read it. This cannot be done, because even large creditors who value their reputation primarily protect their personal interests. It is important to pay attention to the subtleties of calculating penalties, the obligations of the parties, the conditions for early payment and the subtleties of charging commissions for financial transactions. In addition, you should not refuse insurance, because in this case the interest rate increases.

- We receive money and repay the loan. After transferring the funds, we save the receipt. When applying for a targeted loan, you will have to report costs to the credit institution. The financial institution provides a payment schedule that must be strictly followed. Even temporary delays can result in large fines.

Mortgage secured by real estate: how the registration process works

At the first stage, the borrower is recommended to find a financial organization whose conditions suit him best. It is worth seeing whether the property meets the company's requirements. The following are the steps:

- Submitting an application for a loan.

- Receiving a response from the bank, preparing documentation for real estate.

- Assessment of the market value of housing.

- Filling out insurance documents, obtaining a company opinion.

- Review by the bank of a set of documents, making a final decision on the transaction.

- Exit to the signing of the agreement by the borrower. Signing documentation at the company office.

- Registration of the transaction in Rosreestr.

Then the borrower will have to buy insurance from an insurance agent and receive funds from the bank into an account or in cash. Now more about the stages.

After initial loan approval, up to 90-120 calendar days are given to collect documents, depending on the bank. But a person can enter into a deal earlier. Some companies give a discount on the annual rate for a quick deal.

Ordering an estimated cost is a mandatory procedure . Some banks take it upon themselves, but most lenders leave it to the borrower. The client can choose a third-party firm for the assessment or enter into a contract with a bank partner.

Third-party firms are usually chosen by people who doubt that the bank partner will indicate the real cost of housing. The report is drawn up in two copies, one of which remains with the borrower, and the second is sent to the bank. From the moment of payment, the documents will be prepared within three working days.

Next, the person fills out documentation for insurance at the agent’s office. The company issues a conclusion and determines the amount of the premium. The borrower may refuse life and health insurance according to the law. Insurance is not always necessary. There are strict restrictions on insurance cases that must be read carefully when concluding a contract.

On a note! It is recommended that you read all footnotes and fine print from the insurance contract.

After receiving a set of documents for real estate, the bank makes a decision and offers final terms for the loan - amount, interest rate, etc. The personal manager coordinates a meeting with the client - place, date, time. The bank opens a current account in the client's name.

If the property being purchased is mortgaged, an account is opened in the name of the seller. And on the day of the transaction, the contract will be signed not only by the borrower, but also by the seller.