Line of mortgage programs

VTB Bank offers mortgage lending to borrowers of any category.

A mortgage in its broadest sense involves obtaining funds secured by real estate. Such a loan can be used for the purchase of housing or part of it, as well as for the construction of a house, repairs or any other purposes, while the borrower has the right to provide existing or purchased housing as collateral.

As one of the leading banks in the field of housing lending, VTB 24 offers its clients a wide range of mortgage services:

- “New building” – a loan for the purchase of housing under construction or already built, but not registered;

- “Secondary housing” – a loan for purchasing an apartment on the secondary real estate market;

- refinancing – a program for transferring a mortgage loan from a third-party bank on more favorable terms;

- military mortgage – for participants of the military savings-mortgage system (NIS);

- “Secured by real estate” – a large loan for any purpose, issued secured by existing real estate;

- “Pledged real estate” is a program for the purchase of an apartment, house or plot that is pledged to the bank.

Additional options for potential consumers:

- “Victory over formalities” – the opportunity to apply for a housing loan with a minimum of documents by increasing the rate and down payment;

- the use of maternity capital is an option for a young family with two or more children, which allows you to get a mortgage from VTB with virtually no down payment, using a certificate for maternity capital;

- “More meters - lower rate” is a special VTB program that allows you to reduce the loan rate when purchasing an apartment in a new building or in a secondary building with an area of 65 square meters or more. m.

Employees of JSC Russian Railways who need to improve their living conditions can receive a corporate subsidy and apply for a mortgage for railway workers at VTB 24 on preferential terms and without a down payment. Details are on the company website www.zdi.ru.

Mortgage programs

VTB has been providing lending for many years, so it has managed to develop mortgage products that are in demand among different categories of citizens. Each program has its own characteristics and limitations.

Buying a home

Refers to the classic mortgage program, which is available to every citizen. It does not offer benefits, but due to its affordability, 40% of borrowers choose it.

The general conditions are as follows:

- Rate – 10.7% – 11%;

- Down payment – 20%;

- Amount from 600 thousand rubles for 30 years, regardless of whether it is primary or secondary housing.

This type is available in rubles or other currencies offered by the bank.

Mortgage without proof of income

It is not necessary to have an official income in order to get a large loan to purchase real estate. Citizens who are unable to document their income must make a down payment of 30-35% of the price of the property on the market. In this case, the chances of receiving a positive answer increase.

Due to the fact that the banking institution is at significant risk, the conditions for obtaining a mortgage at VTB are becoming more stringent. Every month, citizens will be forced to pay a high percentage when compared with officially employed clients.

More meters less rate

The positive thing about this type of lending is that the loan is issued for cozy and spacious apartments with an area exceeding 65 sq.m. This program is used most often by families with children.

Standard conditions:

- The amount is up to 60 million rubles;

- Percentage – 9.2%;

- Down payment – 20%;

- The loan itself is taken for 30 years.

Look at the same topic: How to get a mortgage from Surgutneftegazbank in [y] year? Terms of mortgage programs and bank rates

But there is one nuance in the form of mandatory registration of comprehensive insurance. You should also pay a down payment in the amount of a quarter of the loan amount.

Military mortgage VTB 24

Persons liable for military service, serving in the army or working in law enforcement agencies can participate in the savings-mortgage system. Every year this category of people counts on benefits and benefits. These funds are targeted, so the money can be used to pay off the mortgage. But there is one caveat: clients with 3 years of military service experience are allowed to participate in the program.

Mortgage for salary clients

Citizens who are already clients of the bank and receive wages through it have privileges. To obtain a mortgage, you do not need to prove your solvency or bring additional documents. During the period of cooperation, the bank itself can offer people favorable offers. The interest rate is 10%, and the money is borrowed for 30 years with a down payment of 10%.

VTB mortgage with government support

This banking support was created with the help of the state to provide less protected segments of the population with real estate. Depending on the status of borrowers, benefits are calculated for them. There is one drawback: a mortgage with government support requires a long process of filling out an application and concluding a deal, which can take several weeks.

Mortgage for young families

Spouses who have not reached 35 years of age belong to the category of a young family. A profitable mortgage is available to them from VTB under a preferential program. Instead of the initial payment, the couple can pay a subsidy from the state. If a couple has a child, the contribution amount will be 40%, and childless couples pay 35%.

Mortgage using maternity capital

Maternity capital is an auxiliary amount for mothers who have given birth to more than one child. Payments of targeted state assistance are made when the child reaches three years of age. But, if the money is transferred to pay the mortgage, you can not expect to reach this age. VTB allows you to pay the first installment or existing debt with maternity capital.

Mortgages for young professionals

To support the development of science, the state creates favorable conditions for beginners and specialists. VTB 24 clients can obtain a loan at a reduced annual rate with the ability to pay off the debt over 30 years.

Collateral property

This program involves a loan for the purchase of residential property that is pledged and subsequently sold.

General terms and Conditions:

- Interest – 10.6% exclusively on collateral property;

- Down payment of 20%;

- A loan of up to 60 million rubles is issued for terms of up to 30 years.

The financial service is unprofitable due to lengthy legal decisions.

Refinancing

Refinancing at VTB Bank is offered according to the following requirements:

- The constant percentage is 8.8%;

- The mortgage loan is refinanced exclusively in Russian rubles;

- The loan is 80% of the purchased property;

- The terms are 30 years.

You can repay the loan early, and no penalties will be imposed.

Terms and rates

Table: comparison of conditions for bank mortgage programs.

| Name | Min. — max. amount, rub. | Bid | Max. term | Original contribution, % of the cost of housing |

| New building | 600 thousand – 60 million | From 9.1% | 30 years | 10% |

| Secondary housing | 600 thousand – 60 million | From 9.1% | 30 years | 10% |

| Refinancing | Up to 30 million, but not more than 80% of the property value | From 8.8% | 30 years | — |

| Refinancing according to 2 documents | Up to 30 million, but not more than 50% of the property value | From 10% | 20 years | — |

| For military personnel | 2.435 million | From 9.3% | 20 years | 15% |

| Secured by real estate | 15 million, but not more than 50% of the value of the property | From 11.1% | 20 years | — |

| Collateral property | 600 thousand – 60 million | From 9.6% | 30 years | 20% |

| Victory over formalities | 600 thousand – 30 million | From 9.6% | 20 years | 30% |

| More meters - less rate | 600 thousand – 60 million | From 8.9% | 30 years | 20% |

The interest rate on mortgage products is presented in a minimum value, since its final amount is influenced by the following factors:

- client category (salary client, employee of a budget institution);

- provided package of documents;

- insurance conditions.

The available loan amount is calculated based on the borrower’s income. The amount can be increased by attracting co-borrowers (up to 4 people).

It is also permissible to increase the level of trust of the bank with the help of additional collateral - guarantors. The spouse of the acquirer must become a co-borrower or guarantor for the loan, unless a prenuptial agreement was previously concluded between them, releasing one of the parties from debt obligations and rights to real estate.

When applying for a loan under the “Resale Housing”, “New Building” and “Loan Secured by Real Estate” programs, the client transfers the purchased or owned housing to the bank as collateral. To do this, the lender will draw up a mortgage agreement, which will give him the right to dispose of the property in the event of long-term arrears on the loan.

Currently, the practice of drawing up a mortgage agreement or pledge agreement is an alternative to drawing up a mortgage for an apartment. In this regard, the borrower will receive a certificate of ownership marked “encumbered,” which will not allow him to sell, donate, or exchange the property until the debt is fully repaid.

Types and general conditions of VTB mortgage programs

- Mortgage with state support at 5%. It assumes full insurance and a 5% rate during the grace period, according to the program “for the second and third child born on January 1, 2018.” The borrower must contribute up to 20% of the cost of the property (the use of “maternity capital” is allowed). At the same time, the amount of financial assistance ranges from 500 thousand to 12 million rubles. (depending on the region). Grant period up to 30 years;

- “Mortgages for the military. Having 15% of the cost of the apartment, a serviceman can take out a mortgage of up to 2.999 million rubles. at 8.5% per annum, paying off the debt over 25 years. The military member must be under 50 years of age at the time of loan repayment;

- "Collateral housing." Bank clients can purchase residential space owned by the bank as collateral and put up for sale at 8.8% per annum. They can allocate from 600 thousand rubles for the purchase. up to 60 million rubles The loan is provided for 30 years. When concluding a transaction, it is necessary to deposit at least 20% of the cost of the purchased property;

- "New building". For housing in new buildings, the bank provides clients with between 600 thousand and 60 million rubles. (from 7.9% per year). Down payment from 10% of the cost. The mortgage payment period is up to 30 years;

- "For secondary housing." The terms and rates are the same as for mortgages for new buildings;

- “More meters - lower rate”, allowing you to reduce the rate from 8.1% per annum, provided that the apartment area is from 100 sq. m. m;

- “Mortgage refinancing” (for our clients and clients who have taken out a mortgage with another bank). At a rate of 8.5%.

Details on mortgage programs on the page.

All mortgage programs at VTB 24 take into account not only the insurance of the property, but also the voluntary insurance of the borrower. If you refuse to insure your life, an increase in the interest rate and possibly the down payment is allowed.

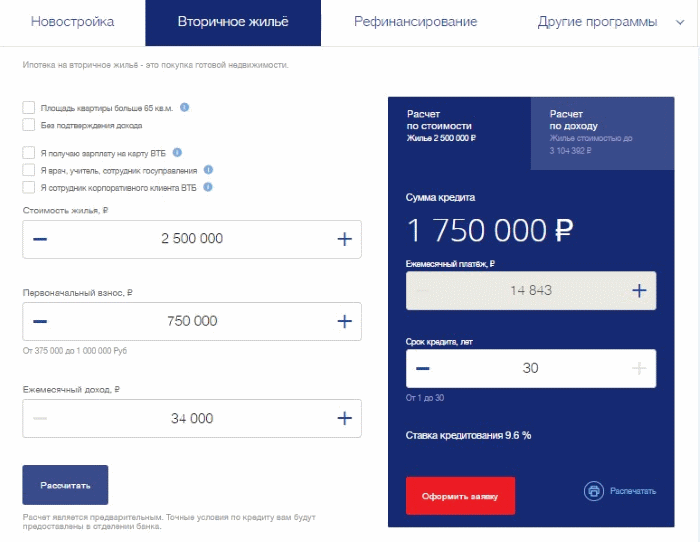

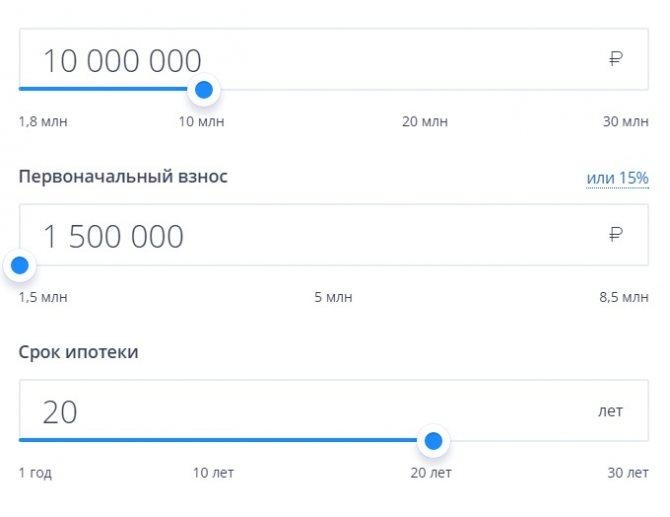

Mortgage calculator

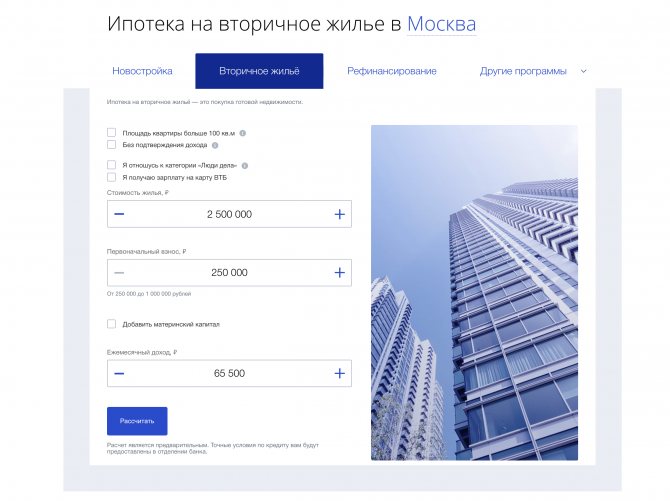

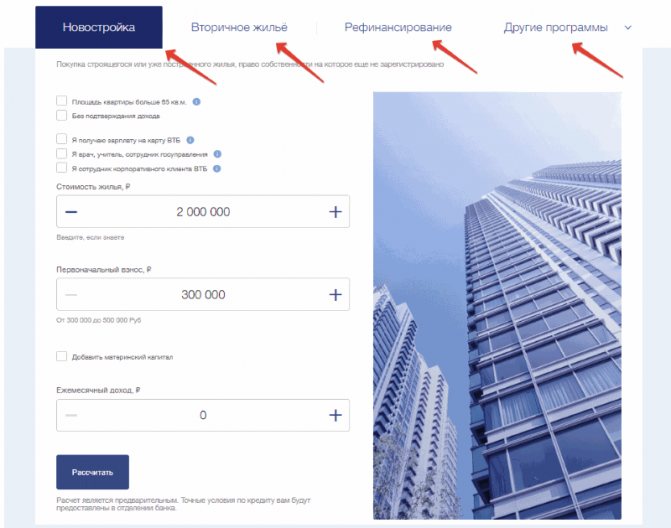

To get an idea of the cost of a mortgage, you can make a calculation using a calculator on the official website of VTB 24. The program determines the interest rate, the size of the monthly payment and the available loan amount based on the client’s income.

Go to the calculator to calculate the amount on the VTB website

The calculator takes into account the following parameters:

- client category;

- the ability to provide documents on income;

- housing costs;

- the amount of the down payment;

- amount of income;

- payment period;

- comfortable monthly payment amount.

Calculate your future loan payment without going to the branch.

To calculate the cost of a mortgage online, just visit the official website of VTB 24 and select the desired home lending program on the appropriate tab. The calculator will appear on the page describing the program conditions.

The mortgage calculator on the VTB 24 website provides a preliminary cost calculation. The program does not take into account the availability of maternity capital or insurance conditions. To obtain an accurate calculation, you should contact a bank branch or the CEC (Mortgage Lending Center).

Submitting an online application for a mortgage at VTB 24.

Fortunately, technology does not stand still, so when searching for a lender to apply for a mortgage, you do not need to visit a branch. All information can be found on the official websites of banks. Here you can submit a preliminary application for a mortgage to find out a preliminary decision. Now you can apply for a cheap mortgage:\

Application for a cheap mortgage

- Mortgage amount up to 100 million rubles

- Duration up to 25 years

- Rate from 11.2% per annum

- Down payment from 15%

- Mortgages for young families and for maternity capital

- Quick consideration of the application and receipt of a decision

- Professional approach, assistance in paperwork

- Minimum red tape and trips to the bank

Apply now

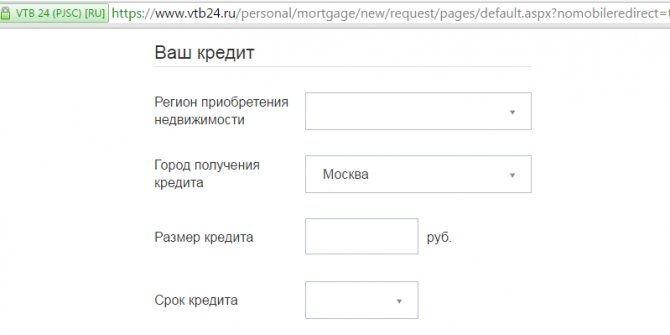

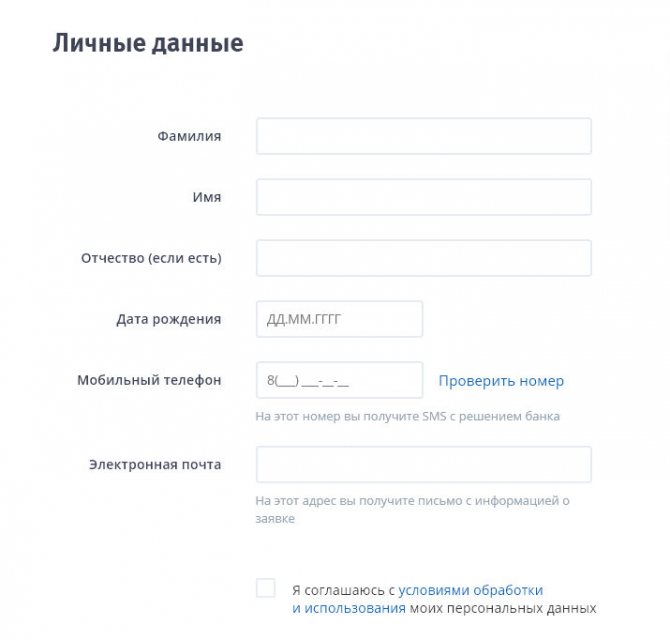

You can also submit an online mortgage application on the VTB 24 website. To do this you need:

- Follow the link for VTB 24 online application.

- Fill out the field with personal data: enter last name, first name, middle name, mobile phone number where you can contact.

- In the field about loans, mark the information about the region where the property was purchased and the city (select from the drop-down list). Enter the amount and term (from the list) yourself from 5 to 30 years in 1-year increments.

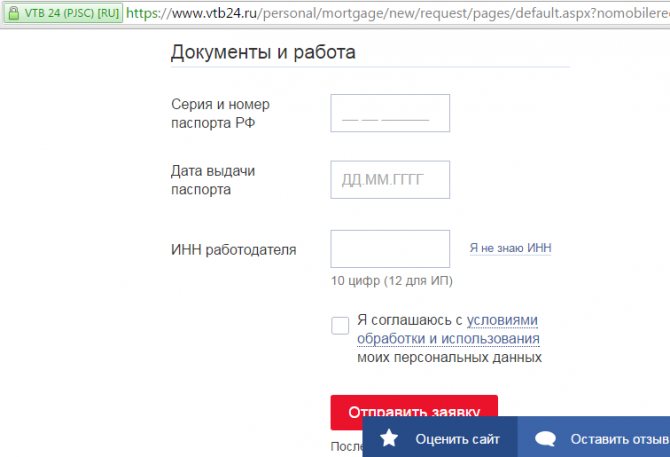

- In the Documents and work section, enter the series and passport number, TIN of your employer (10 characters or 12 characters for individual entrepreneurs)

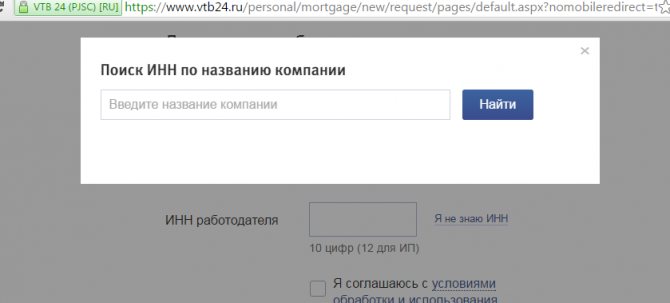

- If the borrower does not remember or does not know the TIN, then you can enter the name of the organization and select the appropriate one from the drop-down list.

- After filling out all the fields, you need to check the box indicating consent to the processing and use of personal data. Consent can be revoked by writing a written statement at a bank branch.

- Submit your application for consideration. Usually, within 24 hours, a bank employee calls you back on the specified phone number and advises you on the issue of providing documents and bank requirements. He will also be able to provide the missing data.

- If, after the initial analysis, the client receives a conditionally approved decision, then he will need to come to the office with a package of documents: passport, a second one of your choice (SNILS, INN, driver’s license), 2NDFL or a certificate in a special form, a copy of the work record certified by the company, where the client works.

Required documents

The list of documents for obtaining a mortgage at VTB 24 depends on the selected program. To submit a preliminary application on the website or in a branch, a potential borrower only needs to have one document with him - a passport.

To receive a final decision on issuing a loan under standard conditions, you need a full package of documents and certificates:

- passport;

- SNILS;

- a document confirming employment (a copy of the contract, a certified copy of the employment record or an extract from it, a copy of the contract for military personnel);

- document confirming solvency (2-personal income tax, certificate from employer, certificate in bank form, declaration for individual entrepreneurs, salary account statement);

- military ID for men under 27 years of age;

- migration card, visa and residence permit for foreign citizens.

For VTB salary clients, proof of income is not required. When applying for a loan to military personnel who are NIS participants, no records of solvency are kept.

Mortgage under 2 documents

Documents for obtaining a loan under the “Victory over formalities” program:

- passport;

- SNILS or INN.

Conditions:

- Mortgage amount from 600,000 rubles. up to 15,000,000 rub. (for regions). For Moscow and St. Petersburg up to RUB 30,000,000.

- The mortgage term is 30 years.

- The interest rate is 13.6% per annum.

With a simplified package of documents, the client can receive a loan only for the purchase of a secondary or new building, as well as refinance a housing loan from another bank.

What documents are required?

- For Russian citizens, you must provide a passport.

- If the borrower is a foreigner, then, in addition to a passport, you need a visa or other certificate indicating the legality of your stay in the country.

- The work record book can be provided in the form of a certified copy. If guarantors are provided, they also certify work books or employment contracts.

- Documents on income are provided either in the form of a bank or an accounting certificate with the seal and signature of the employer.

The manager may also ask for copies of documents for the purchased apartment.

If the borrower plans to use maternity capital, then the following will be required: a certificate from the Pension Fund, a child’s birth certificate and a marriage certificate.

The “Victory over formalities” credit project provides for obtaining a mortgage using only two documents: SNILS and a passport. Under this program, VTB 24 provides loans of up to 30 million rubles.

Calculating overpayment on a mortgage calculator

The site has a calculator that allows you to set up annual rates, payment terms, and monthly payments. After the analysis, you can immediately proceed to filling out the questionnaire by clicking the “Fill out application” button. Using this tool, the overpayment for the entire period of the loan agreement is calculated, the amount of payments broken down into repayment of the principal debt and accrued interest.

Requirements for the borrower

- Age – from 21 to 65 years at the date of loan repayment.

- Citizenship and place of registration – without restrictions.

- Employment and length of service – permanent official employment in the Russian Federation with an experience of at least 6 months, with a total official experience of at least 1 year.

- Ability to confirm income for the last six months.

VTB also extends the requirements for the borrower to his co-borrowers and guarantors, since these persons will be jointly and severally liable for the loan. However, unlike co-borrowers, guarantors will not have to confirm their salary with a certificate - their income is not taken into account when calculating the available loan amount.

VTB 24 Bank allows you to get a mortgage for both employees and individual entrepreneurs who have been running a business for at least 6 months.

General requirements of the bank for the borrower

Citizens who want to get a mortgage at VTB 24 must meet the following requirements:

- Russian citizenship is not necessary, i.e. Even foreigners who legally reside in the Russian Federation can get a loan;

- good credit history;

- official employment;

- total work experience - from 1 year , in the current place - more than 3 months ;

- 50% The borrower's monthly income must be sufficient to pay the monthly mortgage payment.

The borrower confirms his income with income certificates. To increase the amount of income, VTB Bank allows you to attract up to 4 co-borrowers.

Registration of a mortgage

Stages of buying an apartment on credit:

- Familiarization with the terms and conditions of the bank, collection of documents.

- Filing an application.

- Search for housing that meets the bank's requirements.

- Registration of the transaction: conclusion of a loan agreement, purchase and sale, collateral, insurance.

- Carrying out mutual settlements.

- Re-registration of the title deed, transfer of registered agreements to the bank.

If the preparatory stage has already been completed and all documents have been collected, it is time to submit an application. This can be done in two ways.

- fill out a form on the bank's website.

- contact the department in person.

You can get advice on the conditions and select a program with the help of a specialist by calling the VTB help desk at 8-800-100-2424. The website also has a function for ordering a call back to the applicant’s number.

Online application

To apply for a mortgage online, you need to visit the bank’s official website and go to the tab with home loan programs. Having selected the one you need, you should open a window with its description and find the “Complete” button at the bottom of the page.

Apply on the official website

The online application form differs depending on the program.

The application form indicates:

- Full name and contact details;

- passport details;

- employment information (employer’s tax identification number, length of employment, income);

- information about the apartment being purchased and the planned loan (amount of down payment, type and cost of housing, convenient repayment period, etc.).

Within three hours after sending the questionnaire, a bank employee will call you back at the phone number indicated in it. The specialist will clarify additional information, and after 2-3 days the bank will notify the applicant of the decision on the application.

The answer will be considered preliminary - then the borrower will still have to go to the branch with a full package of documents.

Contacting the department

The application form to obtain a final decision is completed at the mortgage center, and if there is no center in the locality, at any bank branch. If you have a complete package of documents, the processing time for a mortgage application ranges from 24 hours to 5 days. An application for a mortgage under the “Victory over formalities” program is reviewed within 24 hours.

Find a VTB 24 branch

A positive decision is valid for 4 months. This time is enough to find suitable housing or get acquainted with the offers of other banks.

Property selection

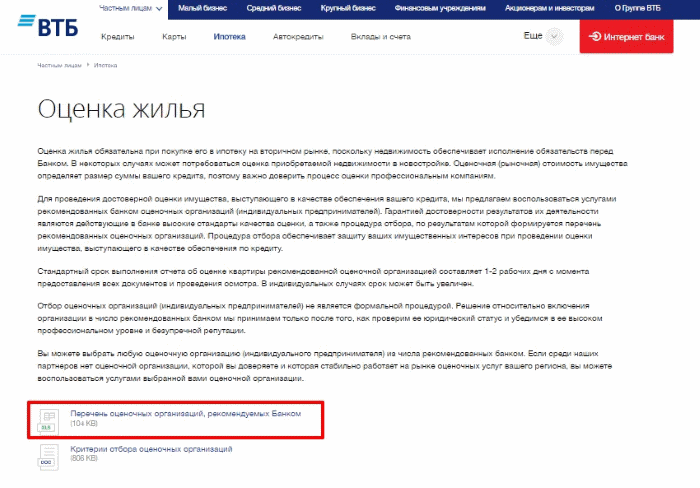

When purchasing a resale apartment, a home appraisal is required.

To quickly and efficiently select an apartment, the bank offers the services of partners: developers and real estate agencies. Cooperation with these companies is carried out on preferential terms, while borrowers have access to an extensive database of objects, and advice from specialists can be obtained at the office of the mortgage center.

Housing assessment is carried out when purchasing real estate on the secondary market, in exceptional cases - when purchasing an apartment in a new building. The result of the assessment determines the amount of the loan provided by the bank, so in this matter you should trust only reliable companies.

At the moment, the bank accepts assessment reports only from accredited partners whose work meets specified quality standards.

Collecting documents regarding the apartment is the seller’s task, since most certificates are provided only to the owner of the property or his official representative by proxy. To speed up the process, you can seek help from real estate specialists.

Making a deal

The procedure for obtaining a home loan consists of signing a purchase and sale agreement and loan documentation, as well as obtaining an insurance policy. At the time of this transaction, all participants must be present at the lender’s office: the seller (if we are talking about a secondary property), the borrower, his guarantors and/or co-borrowers.

The signed documents and the pledge agreement drawn up by the bank are sent to the registration authority. Borrowed funds are transferred to the seller or developer on the same day. Registration of a transaction in Rossreestr lasts from 5 to 7 days.

Having received the registered documents, the buyer submits a notarized copy of the certificate and the pledge agreement to the bank.

A pledge agreement is essentially a mortgage - a security that gives the lender the right to dispose of the pledged object in the event of the borrower’s refusal to fulfill loan obligations.

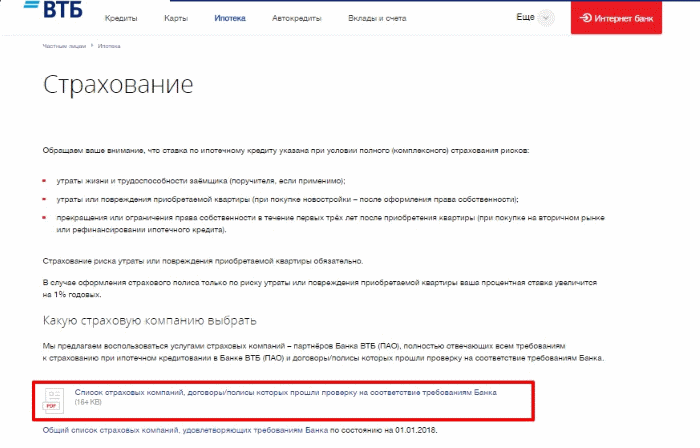

Mortgage insurance

By signing an insurance contract, you protect yourself and your property from various risks.

An obligatory stage of concluding a transaction is the execution of a comprehensive insurance contract. It includes the following risks:

- life and health insurance of the borrower;

- protection of the apartment from loss or damage;

- title protection (property rights).

When applying for a mortgage at VTB, title and life insurance are not required, but if these risks are excluded, the interest rate increases by 1 point. The borrower can enter into a risk protection agreement only with an insurance company accredited by VTB.

You can view the list of partners at the branch or on the lender’s website. This list includes the bank’s subsidiary, VTB Insurance.

The borrower has the right to independently choose an insurance company. If this company is not on the list of accredited partners, VTB is ready to review its services for compliance with the bank’s requirements and standards.

List of insurance companies-partners of VTB

Procedure for obtaining a mortgage

Technologies do not stand still, and today you can take out a loan, even for an apartment, without leaving your home. There is a special VTB online service for this. There you can fill out a form in a few minutes and receive a quick response from the bank.

Applying for a mortgage online

The online mortgage application is a form that must be filled out. This must be done carefully, because incorrect information may affect the bank’s decision.

The following fields must be completed in the online application:

- Personal data. Here the user must indicate his full name, as well as a contact telephone number and email.

- Your credit. In this section you need to indicate the region in which you plan to purchase an apartment and the city in which the loan will take place. In addition, it is important to indicate the loan amount and the approximate repayment period.

- Documents and work. This is the last section. It must indicate the series and number of the Russian passport, as well as the TIN of the organization in which the borrower works.

Finally, you must tick the box indicating consent to the processing and use of data. After this, the application can be sent for consideration. The client's application is reviewed within business days. The decision is communicated by telephone. If it is positive, then a VTB employee will advise on the conditions for issuing a loan, and will also tell you what documents need to be provided.

Redemption

You can repay a VTB loan in one of several convenient ways:

- at the cash desk of any lender's office;

- through remote servicing services - mobile and online banking;

- through ATMs;

- transfer from accounts and bank cards of other banks;

- in communication shops, in Russian Post branches.

If you want to pay your VTB mortgage through third-party organizations, you should independently calculate the payment amount, taking into account commissions, and also take into account the term for crediting funds.

For the client’s convenience, his salary or debit card can be linked to a credit account - then funds for the mortgage payment will be debited automatically.

Payment at a branch or in the offices of third-party organizations can be made either by the borrower himself or by his authorized representative, provided he has a passport and a loan agreement.

VTB 24 allows early full and partial repayment of a mortgage for any period without fees or penalties. When the loan is partially closed, at the borrower's choice, the payment amount is reduced or the payment schedule is reduced at your choice. Full early repayment can be calculated in VTB Online or at a bank branch.

How can I reduce my mortgage rate or payment?

Bank clients have several options to reduce the financial burden on the family budget, both before completing the transaction and after purchasing a home.

- Apply for a mortgage loan under the “More meters - lower rate” program.

- Transfer salary receipts to a VTB card.

- Use maternity capital to partially repay the loan.

- Apply for a tax deduction for the purchase of a home or for paying interest on a mortgage loan.

- Take advantage of the borrower support program from the Mortgage Lending Agency (AHML).

In addition, from September 1, 2020, VTB has the opportunity to reduce the interest rate on mortgages issued earlier. To take advantage of this offer, you must meet several conditions:

- at least 12 payments must be made on the loan;

- the interest rate specified in the contract upon registration is 12% or more;

- According to the agreement, there should be no current overdue payments or closed delinquencies for more than 30 days.

To take part in the program, you must contact the Central Election Commission to fill out an application for a reduction in the interest rate on your existing mortgage. In response, the bank is ready to increase the loan term and reduce its cost to 10%.

To apply for refinancing, you must again order a housing assessment report and pay a fee (6 thousand rubles for residents of the regions, 12 thousand for Moscow and Moscow Region). This program does not allow AHML borrowers, as well as those who have taken out non-targeted mortgage loans, to participate.

At the moment, the mortgage interest rate reduction program from VTB 24 is temporarily unavailable.

Video: Pros and cons of refinancing a mortgage.

Review of mortgage lending programs from VTB

More meters, less rate. This program is beneficial for those who buy a large apartment, from 65 m2 . For such clients, the bank reduces the rate by 0.5% . Thus, you can save on overpayments and purchase more spacious housing. The down payment must be at least 20% of the loan amount.

Buying a home. You can buy an apartment in a new building or on the secondary market. This program is interesting because it requires a smaller down payment - from 10% . The size of the contribution depends on the term and the chosen amount; you can make an approximate calculation on the VTB website.

The amount of the contribution depends on the price of the apartment and the term of the mortgage.

Victory over formalities. To take out a mortgage under this program, you will only need two documents: a passport and SNILS. Instead of a pension certificate, you can provide a TIN. Your application will be reviewed as soon as possible, and you will receive within 24 hours.

The rate for this program is 0.7% . The down payment when purchasing on the secondary market must be at least 40% of the apartment price, for new buildings - from 30% . Maternity capital cannot be used as a down payment.

Refinancing. If you previously took out a mortgage from another bank, your debt can be transferred to VTB on more favorable terms. This way you can reduce your monthly payment. The rate will be further reduced for some categories of clients (salary project participants, doctors, teachers, civil servants).

To refinance your mortgage, submit an application from the website. After a call from a bank employee, you need to come to the office in person with your passport, income certificate and all documents related to the old mortgage. A contract will be concluded with you on new terms.

Military. This type of mortgage is available only to military personnel of the Russian Federation who have become participants in the savings mortgage system. The NIS program includes military personnel who entered into a contract after 2005. You can get a mortgage three years after joining the system.

Collateral real estate. The program is aimed at purchasing apartments that are for sale and are pledged to the bank. You can buy an apartment in a new building or on the secondary market, a townhouse, a private house or a plot. Select a property from the list on the VTB website and send an application to the bank.

You can choose a suitable apartment directly on the VTB website.

Loan secured by existing housing. You can get a loan for any purpose using your existing apartment as collateral. It must be located in an apartment building within the city. The loan amount cannot exceed half the value of the property. The apartment of the borrower, spouse or relative can be used as collateral (in this case a guarantee is required).