Determine the structure of the future budget of income and expenses

Approval of the estimate of income and expenses of the owners' association for the next year falls within the competence of the general meeting of HOA members in accordance with Part 8.1 of Art. 145 Housing Code of the Russian Federation. This issue is one of the mandatory issues for discussion by members of the partnership at the PSC.

The form of this document is not fixed at the legislative level, therefore each HOA draws up its own estimate of income and expenses. The structure of the estimate is dictated by the content, which is also not clearly stated in the regulatory legal acts.

The estimate of the HOA is developed and submitted for approval by the general meeting of members of the partnership by its board (Part 3 of Article 148 of the Housing Code of the Russian Federation). This must be done annually. At the same time, the audit commission of the HOA must also present its conclusion on the compiled estimate (clause 2, part 2, article 150 of the Housing Code of the Russian Federation).

Formulate the content in accordance with the requirements of housing legislation

The content of the estimate, which dictates the structure of the document, is not directly regulated and not enshrined in one legal act. The estimate of income and expenses includes work and services for maintaining the house specified in the Housing Code of the Russian Federation, RF PP No. 416, No. 491, No. 290, 410, and Resolution of the State Construction Committee of the Russian Federation No. 170.

Clause 33 of RF PP No. 491 states that the estimate of income and expenses includes the maintenance of the common property of an apartment building, as well as utility resources for the maintenance of the property owners. Utility resources supplied to the house to provide utilities to residents are not included in the estimate from 2020.

The Housing Code of the Russian Federation provides a wider list of items for the estimate. According to Art. Art. 137, 145, 150, 158 of the Housing Code of the Russian Federation, the estimate of expenses and income of the HOA includes work and services for managing the house, maintaining and routine repairs of the common property of the apartment building, including the supply of utility resources for its maintenance.

Targeted financing funds are not included in the estimate: for example, payments for major repairs of apartment buildings and subsidies allocated from the budget (clause 14, clause 1, article 251 of the Tax Code of the Russian Federation).

How to compose it correctly?

The estimate can be in any form. The main thing is that its format is approved by the management of the HOA and approved as convenient for filling out and maintaining reporting activities.

There can be three types of estimates in an HOA:

- Consolidated - reflects the costs of restoring or modernizing the entire building and its ancillary premises.

- Object - it contains information about the costs of one room.

- Local - reflects information about the cost of restoring a specific unit in a building or in the area adjacent to it.

Not a single amount indicated in the estimate should be written down without the addressee to whom it will be transferred or the source of receipt of funds.

Advice! In a situation where the partnership does not conduct business at all, there is no point in drawing up an income budget, since the organization’s funds are determined by the cost estimate.

Initial data when drawing up a budget

When drawing up the HOA budget, take into account:

- Budget size for previous years (period from 1 to 3 years).

- The technical condition of the supervised facility (in this case, the report indicates the total area of premises occupied by residents, the size of facilities that are not subject to occupancy and their purpose, the number of floors in the building, the presence and condition of elevators, the number of beneficiaries paying for utilities at a reduced rate).

- Regularity of funds received.

- Inflation rate.

- The amount of costs for the planned modernization/repair of the building, objects listed on the balance sheet of the HOA.

- Costs of paying for the services of hired HOA personnel.

- Costs for maintenance and management of housing stock.

- The amount of funds on the balance sheet remaining from the savings of the past period.

- The amount of building materials and other resources of this kind remaining after previous work.

The expense report must reflect every movement of funds in connection with maintaining the technical condition of the house, its maintenance, cosmetic and major repairs of the common property of the residents of the house.

Reference! The HOA estimate includes all transfers of funds on behalf of the HOA and payments under the terms of contracts with home service providers.

Expenditure part

The expenditure part of the budget, that is, the cost estimate, consists of the following items:

- Expenses for the management staff of the HOA:

- salary for hired personnel officially hired;

payments under social insurance programs;

- payment of office bills (electricity, water, heating, communications);

- inviting consultants;

- ensuring management of office equipment, furniture, computers;

- advanced training courses for management employees;

- fees for participation in club programs;

- commissions of banking institutions;

- entertainment expenses.

- Cost items for maintaining a house in proper technical condition:

- salary of personnel performing direct tasks of maintaining general facilities;

- payments to social services funds;

- maintenance of the house and surrounding areas by HOA employees or invited teams;

- purchase of building materials and equipment;

- common house utilities;

- maintenance of technical condition, repair of fixed assets;

- insurance obligations;

- land tax payments.

- Expenses for repair work of common property:

- ongoing work to restore the technical condition of the house structure;

- ongoing work to restore the technical condition of utility lines;

- overhaul.

- Expenses for transfers to funds:

- for restoration, replacement of fixed assets;

- savings account for current repair work;

- savings account for major repairs;

- reserve account for unexpected needs;

- accounts for bonus payments;

- savings account for financial support.

Describe in detail all areas of planned expenses for the next year.

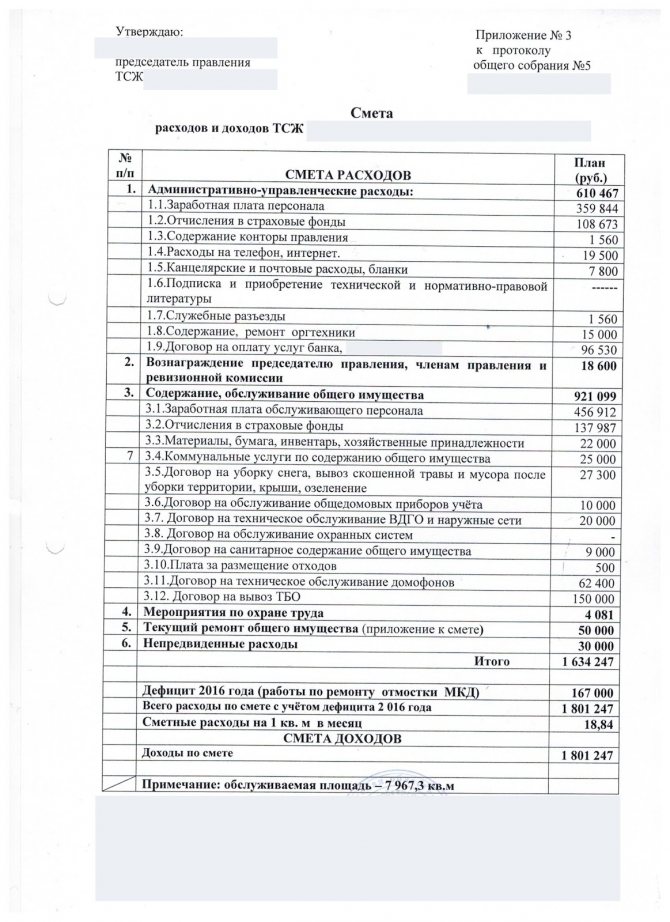

The structure of the “Expenses” section in the estimate of income and expenses of a homeowners’ association will be more complex, since the HOA performs a wide range of work and provides many services for the proper maintenance of the common property of the owners of premises in an apartment building.

All HOAs include in their expenses funds that are planned to be spent next year on:

- carrying out work on the maintenance and repair of the common property of the apartment building in accordance with the requirements of the Housing Code of the Russian Federation, RF PP No. 416, No. 491, No. 290, Resolution No. 170;

- provision of housing services for the supply of CR to SOI;

- expenses associated with the work of the owners' association: office, transport, personnel, housekeeping, payment for services of banks and payment centers, etc.;

- taxes, fees, and fines paid by the HOA itself.

The HOA's expenses may include funds to resolve unforeseen situations if they have happened before and there is no guarantee that they will not happen again. These are optional expense items, such as, for example, payment for the services of a security company, intercom maintenance, and additional landscaping of the yard.

Types of expenses

Each HOA has a number of mandatory expense items:

- Settlements with the water supplier, the organization that provides water heating.

- Payments to the electrical supplier.

- Maintenance of community owned property.

- Maintenance of local lands.

- Current modernization, restoration of the technical condition of common property.

- Purchase of consumables.

- The needs of the HOA office (paper, office supplies, payment for hired employees, if any.

- Taxes.

Possible and some additional costs:

- insurance;

- loans;

- legal costs.

Attention! If the HOA has not only internal, but also external financial income (subsidies, donations) and the object controlled by the management is in satisfactory technical condition, a prerequisite is created for reducing the amount of contributions of apartment owners.

Bring into compliance the estimate and annual plan for the maintenance and repair of the common property of the house

Separately, mention should be made of such an expense item as the maintenance and current repairs of the common property of the owners. The homeowners' association, along with an estimate of income and expenses, draws up an annual plan for the maintenance and repair of residential apartment buildings.

Like the estimate of income and expenses, the annual plan is drawn up by the board of the HOA and approved at the general meeting of members of the partnership (clause 8, part 2, article 145 of the Housing Code of the Russian Federation). The form and structure of the plan are not established by law: in general, they correspond to the structure of the estimate in terms of the partnership’s expenses for routine repairs of the facility.

Thus, the plan is a list of works and services for maintenance and repairs that the HOA plans to implement in the house. The plan indicates the name and type of work, unit of measurement, cost and frequency. If the work is performed with the involvement of a contractor, then you can indicate its name.

The amounts and list of work included in the cost line of the HOA estimate for routine repairs of common property must correspond to the amounts and work specified in the annual plan for the maintenance and repair of the OI MKD. Typically, such a plan is fully included in the estimate of income and expenses of the HOA.

Features and terms of approval

The procedure for approving the BS is approved by the superior or chief manager of budget funds. The document is approved within 10 working days from the moment when the limits of budget obligations were brought to the government institution.

If the activities of a state institution involve state secrets, then other requirements apply. BS with state secrets are approved no later than 20 working days from the date of delivery of the LBO.

The BS is approved either by the manager himself or by another person who is authorized to perform such actions. GRBS has the right to provide these powers for another person.

The document, which is approved according to the established rules, must be sent to GRBS no later than the day following the day on which the estimate was approved.

Submit an estimate of income and expenses for inspection by the Audit Commission

In accordance with clause 2, part 3, art. 150 of the Housing Code of the Russian Federation, at the general meeting of HOA members, together with the estimate of income and expenses and the annual plan for routine repairs of common property, the audit commission of the HOA must present its conclusion on the estimate.

The Audit Commission must present at the general meeting of HOA members a report on the implementation of the estimate of income and expenses for the past year and an analysis of the estimate drawn up for the next year. To do this, the chairman of the partnership must transfer the prepared documents to the members of the audit commission.

The Audit Commission is obliged to check whether an estimate of income and expenses for the next calendar year has been drawn up, the validity of the calculations made for each item of income and expenses, and the validity of the calculation of the amount of payment for the maintenance of residential premises made on the basis of the estimate.

Approve the estimate of income and expenses at the general meeting of HOA members

After the HOA board has drawn up an estimate of income and expenses, and the audit commission has checked it and made a conclusion as a result, the documents are submitted to the general meeting of members of the homeowners association.

The PSC of the owners' partnership is convened in the manner prescribed in the Charter of the partnership (Part 1 of Article 145 of the Housing Code of the Russian Federation). In order for the general meeting of members to take place, members of the HOA must take part in it, having 50% + 1 votes of the total number of votes of the members of the partnership.

The number of votes of each participant is determined in accordance with the area of the premises owned by him, in relation to the total area in the house owned by all members of the HOA.

In order for the estimate of income and expenses presented by the HOA board to be accepted, a majority of the total number of votes of the HOA members present at the general meeting must be cast “for” (Part 4 of Article 146 of the Housing Code of the Russian Federation).

Place the finished estimate in the GIS Housing and Communal Services

Drawing up an estimate of income and expenses for the year is mandatory for all HOAs and occurs in accordance with the requirements of the Housing Code of the Russian Federation and other legal acts:

- The HOA board draws up an estimate and sends it to the audit commission for inspection.

- Based on the results of the audit, the Audit Commission draws up a conclusion.

- The estimate and conclusion of the audit commission are submitted to the general meeting of HOA members.

- The general meeting of HOA members approves the estimate of income and expenses.

- The HOA places an estimate in the GIS Housing and Communal Services in accordance with clause 17 of Section. 10 No. 74/114/pr.

Based on materials from the RosKvartal portal.

Estimate in the electronic budget

Federal government agencies are required to reflect the BS in the Electronic Budget system if their activities do not involve state secrets. Regional and municipal organizations are not required to maintain documentation in an electronic database, but sometimes GRBS require maintaining an electronic version of the BS.

The Internet system is designed to achieve transparency, openness and accountability in the activities of institutions and to improve the quality of financial management. In 2020, all organizations must fill out estimates in the system.

It is necessary to apply economic calculations and justifications. We make adjustments to the indicators in the same way no later than 10 working days from the date the LBO is delivered to the recipient. Now only GRBS, and not a higher-ranking manager, has the right to approve the clarifications made.