Mortgage assignment: why is it necessary?

The borrower can transfer ownership of the property to a third party, and at the same time transfer the rights and obligations to the bank to service the mortgage loan.

The issue of assignment of the rights and obligations of the mortgagee may arise in various situations:

- After a divorce, one of the spouses renounces his share in the jointly acquired property, while all loan payments are paid by the second spouse, who still owns the property.

- Urgent sale of real estate. If the borrower needs to close the loan and sell the property in a short time, he can do this under an assignment agreement. Typically, this procedure takes less time than early repayment of the loan, removal of the encumbrance and sale.

- Receiving an inheritance. After the death of the borrower, his heir inherits not only the ownership of the property, but also the responsibilities associated with servicing the loan agreement.

- The borrower wants to close the mortgage, for example, due to the inability to repay the debt.

- The lender assigns the loan to another legal entity. This can be either as part of the sale of a mortgage portfolio, or as part of the sale of a loan to a collection company due to the borrower’s failure to fulfill its obligations.

Bank permission

The only case where a borrower can dispose of collateralized property without asking the bank’s approval is in a will. All other operations related to the transfer of ownership of real estate that is under mortgage can only be performed with the permission of the lender.

Therefore, before resolving issues with the potential owner, you must contact the bank with a corresponding application. Banks treat such transactions with extreme caution and issue permission in exceptional cases. If the transaction is carried out in any way without the permission of the creditor, he has the right:

- Carry out a number of measures as a result of which the transaction will be declared invalid.

- Demand early repayment of all debt under the loan agreement, including penalties that were imposed as a result of its violation.

- Carry out the procedure for collecting collateral.

Risks and benefits of the new owner

If the bank does give preliminary consent to the assignment of the mortgage, then the potential borrower will be checked for solvency in the same way as when applying for a loan from scratch. The new potential owner must provide the bank with a complete package of documents, which is necessary to consider the possibility of lending. But it will be easier for him to collect documents than when applying for a new mortgage. There is no need to provide a package of documents for the property, or to evaluate it. This, in turn, allows you to save money. The bank no longer checks real estate documents and a decision can be obtained faster.

In addition, a clear advantage for a new borrower is that the apartment is almost 100% legally clean.

Usually the price of an apartment that is sold by transfer is lower than the market average. But it is necessary to find out whether there are any accrued penalties under the loan agreement. The bank can transfer all fines to the new borrower. If their size is significant, this can significantly reduce the profitability of the transaction. Typically, such issues are resolved by the bank on an individual basis.

Despite all the benefits of the deal, at first glance, it also has a number of risks . The bank does not draw up an additional agreement to the original loan agreement, but enters into a new one. Its terms may differ significantly from the lending conditions of the first borrower. The rate may be increased, the loan term may be reduced, and various fees may be introduced that were not included in the original agreement. All of this significantly increases your monthly mortgage payment. The bank will also require that new insurance contracts be concluded. A new borrower should carefully study all contracts, as they may differ from the standard ones.

If the borrower does not repay the debt, the bank may sell the apartment through an auction, or may transfer rights in favor of a new borrower. Here, a situation is possible when the original owner does not want to voluntarily evict and has to contact the Ministry of Internal Affairs.

The most unpleasant situation that can arise during the assignment of a mortgage is when the former owner goes to court to invalidate the transaction. He can explain the claim by the fact that the transaction was carried out on deliberately unfavorable terms for the seller.

Registration procedure

- A borrower who wants to sell a mortgaged apartment and “get rid” of the mortgage finds a buyer.

- The seller and buyer contact the bank to obtain permission to carry out the assignment.

- The bank checks the potential borrower and makes a decision on the possibility of the assignment.

- A loan and mortgage agreement is concluded between the bank and the buyer.

- The transfer of ownership is registered.

- The buyer pays the seller.

- The new borrower repays the mortgage according to the terms of the loan agreement.

Conditions for the transaction for the assignment of the DDU

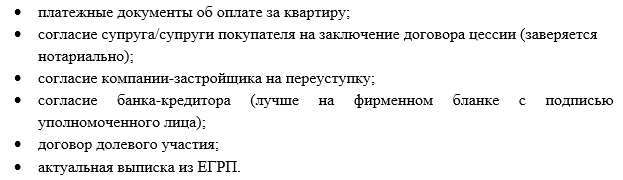

The seller or assignor is required by law to notify the developer of the assignment of its rights in writing. To do this, an application or notification is drawn up in a free format, containing information about the seller and buyer of the residential property, and a copy of the assignment agreement and a set of required papers are attached. Among them:

A new buyer is strongly advised to carefully study the developer's business reputation and history of activities. Only if you are completely confident should you enter into a deal.

The procedure for purchasing an apartment through assignment of the right of claim includes the following steps:

- Informing the construction company and obtaining permission for the assignment.

- Preparation of the required package of documents.

- Concluding an assignment (assignment) agreement and registering it with Rosreestr.

- Concluding a mortgage agreement with a bank.

notifications can be found here. You can download the agreement on the assignment of rights under the DDU using this link.

Transfer of rights to an apartment in a new building

The assignment of property rights is one of the ways to change the owner under a shared construction agreement. The difference with buying a home on the secondary market is that the seller does not have a title document for the property.

Banks are wary of issuing loans for the purchase of an apartment in a building that has not been put into operation. They usually work only with a narrow list of developers with whom they have certain partnership agreements. Therefore, if a person wants to purchase an apartment in a new building, then it is worth finding out which bank the development company works with.

The procedure for drawing up the contract will depend on whether the original buyer has paid the developer in full or in part. If the settlement has occurred in full, then the construction company’s permission for the assignment is not required.

For the buyer, the main risk of purchasing such real estate is associated with the developer. No one can guarantee that the house will be successfully completed and put into operation, especially within the initially stated time frame. In this case, there is a risk of being left without an apartment, but with a mortgage loan. The higher the percentage of construction work is completed, the lower the risk of not getting housing.

Documents for obtaining a mortgage

Next, you need to clarify the amount of your mortgage debt to the bank. To do this, you can contact the office of the credit institution for the appropriate certificate. Each bank sets its own requirements for documents in order to consider your application. And this list can vary greatly. But some points are the same for all banks.

By the way, contractors who work for the developer can also act as sellers of apartments for assignment. Alexander Ginovker tells how to assess risks if the contract is issued to the contractor as a legal entity. It is important that the contractor fulfills his obligations to the developer and that all documents are available. But our desires do not always coincide with our possibilities. However, material problems, in this case, can be solved. If you do not have the required amount on hand, you can always purchase an apartment in a new building under a mortgage assignment agreement. Since many banks will be happy to provide you with this opportunity. And the number of such banks lending for the purchase of housing upon assignment of the right of claim is growing.

Transfer of ownership rights to an apartment, i.e. a transaction for the purchase and sale of an apartment before the construction of a house is completed is called a cession. The assignor (a person who bought an apartment in a new building directly from the Developer, most often an investor) sells, i.e. transfers to the assignee (buyer) the right to receive a new apartment for a higher fee than he purchased from the construction company. The assignment of rights to a mortgage in ordinary cases refers to a certain system in which a client in need of housing buys real estate that is under a mortgage.

It is dangerous to encounter such problems when transferring shares, such as:

- The developer is almost bankrupt. The house may never be built, and you will have to run through the courts to at least get your money back.

- The apartment building was not built according to the design. It will be good if the layout of the apartments is better and it is put into operation, but if not, you will have to be content with what you have.

- Housing takes a long time to build. Long waits are not good for anyone.

- Will meet with double reassignment. Unscrupulous developers may sell the same apartment to several buyers.

- The contract may be invalidated if the developer is not aware that the share has been assigned.

- The main risk is to be left without real estate and without money if the house is never built. For example, the construction committee will prohibit the operation of the facility.

- The developer is fake. The risks when buying an apartment by assignment are high, just like with a construction organization, so you should check licenses and other documents before purchasing.

This is important to know: Consent to gasification of the owner of shared ownership

Despite the fact that the procedure for completing such transactions is simple and quite transparent, there are still certain nuances and associated risks that must be taken into account. The main one is if the house has not yet been completed. You can never be sure that the project will not be frozen and a person will not lose the money invested.

When a scheme for the assignment of rights to a mortgage is carried out, it should be remembered that any lender does not conclude a document that will indicate the assignment, but concludes an additional document for the new borrower.

My brother entered into a contract of agreement for the construction of an apartment in his name. Currently, the house has been rented out, but the developer has not yet issued the keys and documents for the apartment. What can be done to register an apartment in the name of his mother, a disabled person of the 2nd group?

Real estate expert at Advex Corporation. Real Estate" Anna Deloverova assures that the risk of double sales when purchasing apartments by assignment is practically eliminated today: "There are isolated cases of cases being considered in court on the recognition of the priority right to a built apartment, but these construction projects are ten years ago. Now, under equity participation agreements, Rosreestr keeps strict records of old shareholders and new ones. Housing cooperative agreements are not registered with Rosreestr. Here, all responsibility lies with the developer - it is the developer who draws up assignment agreements on his own terms (sometimes this means payment from 50 thousand rubles to 10% of the price of the property).” The next step is to pay off the debt to the bank using the buyer’s funds. This usually happens in the presence of both parties to the transaction, so that the buyer is convinced that his funds are being spent on purpose.

They also pay attention to the registration period, which can reach up to two months. But there are developers who, immediately after drawing up an assignment agreement, hand over the keys to the apartment if the house is already being occupied, without waiting for registration.

For example, many banks issue a mortgage using two documents: a passport and another identification document. For example, a driver's license.

Also in such cases, the buyer is obliged to pay the seller some funds to cover the amounts of various duties for previous periods. The amount of this amount is agreed upon by the seller and the buyer.

The next point is taxes. As part of the Tax Code, the seller transfers a fee of 13% of the difference in value assigned in the DDU agreement and the assignment agreement. In standard cases, in order not to overpay extra funds, sellers insist that the documents indicate an amount less than the actual amount. In the case of mortgage lending, banks do not make such concessions, and you will have to pay tax in accordance with the amount actually received.

Taxation

The assignment agreement is also concluded in order to avoid additional taxation .

When concluding a purchase and sale agreement, the seller is obliged to pay personal income tax to the budget if he has been the owner of the property for less than three years. When participating in shared construction, the difference between the seller’s initial investments and the price for which the apartment was sold is subject to taxation.

However, there are ways to reduce the amount of tax payable:

- In 2020, the seller has the right to a tax deduction up to one million rubles.

- The difference between the sales and purchase prices is subject to taxation. If the sale is made at the original price, then there is no need to pay tax.

The tax must be paid no later than July 15 of the following year, after the sale.

Advantages and disadvantages

Like any other procedure, selling an apartment by assignment has its pitfalls in the form of pros and cons for each party. The advantages lie in obtaining financial benefits for the seller and the buyer from the difference in the price of finished housing and at the construction stage.

At the initial stage, investments in a new building are much less in size than the sale price of the assignment before putting the facility into operation. But a finished apartment, which is purchased under a standard purchase and sale transaction, is an order of magnitude more expensive than its analogue that is still under construction.

This is important to know: Settlement when selling and buying an apartment

Among the disadvantages, we highlight the following nuances that can be dangerous for the buyer:

- difficulties associated with thoroughly checking the purity of the transaction;

- waiting for construction work to be completed in order to use your apartment in a new building;

- the need to control the transaction independently or to involve a lawyer;

- approval of the transaction with the developer (if there is no consent clause, then it is necessary to notify the new shareholder);

- the possibility of the developer refusing to assign or providing consent for a certain price (the amount can range from 1 to 15% of the cost of the apartment);

Buying an apartment on assignment in a new building is beneficial for citizens who have sufficient capital to invest in construction and strong nerves to monitor all the nuances associated with the purchase. After the transaction for the transfer of rights of claim, the buyer will need to independently monitor the schedule for the delivery of the new building. You also need to clearly know what to do when the property is ready - what documents to get from the developer and how to complete it correctly.

The main argument in favor of the seller’s reliability should be the transaction under the Shared Participation Agreement and the reputation of the developer in the real estate market of the selected region.

Assignment at the initiative of the creditor

The assignment of a housing mortgage is also possible at the initiative of the bank. In this case, the bank does not require the borrower’s consent. But he must notify the client of the changes that have occurred. The following information must be provided to the borrower in writing:

- New details for paying the monthly payment.

- Procedure and methods of making monthly payments.

- Changes in the rights and obligations of the parties.

If the borrower has not received notice, the new lender has no right to impose any penalties for late fulfillment of obligations.

You should not agree to take out a mortgage loan when there was initially an agreement on a subsequent assignment . Because the desire of the property owner and potential buyer is not enough, the decision is always made by the lender.

If you still have any questions about the assignment of a mortgaged apartment (including paying taxes), then our online lawyer on duty is ready to promptly advise you.

We renegotiate the equity participation agreement

If, after repaying the mortgage and removing the encumbrance, the seller refuses to enter into a transaction within the time period specified in the preliminary agreement, the potential buyer has the right to go to court and demand a double refund of the deposit or force the potential seller to enter into a purchase and sale transaction. If, after reading the article “On Assignments” (link), you are convinced that buying an apartment by assignment of rights of claim is a legal, uncomplicated and profitable transaction, then perhaps you might have a desire to purchase such real estate.

It is important to understand that the bank, by issuing you a loan on such terms, is taking a risk. Because it doesn’t check your employment and income, and banks don’t like to take risks. The only thing that makes them give up their beliefs is profit. Therefore, your required down payment on your mortgage should be up to 50%, depending on the bank. And also, according to this scheme, you are guaranteed an increased percentage of 0.5 points or more.

Before selling an apartment under an equity participation agreement, the Seller is obliged to pay the Developer the entire amount of debt for the apartment, or the remaining amount of debt can be transferred to the Buyer. For this purpose, an Agreement is drawn up for the transfer of debt to the new owner. This type of apartment sale can be carried out repeatedly, but only until the house is put into operation and the owner receives a transfer deed for the apartment. The sale of an apartment under an equity participation agreement requires mandatory registration with the Federal Registration Service.

This is important to know: Allocation of shares to children in an apartment or house based on maternity capital in 2020