Is it possible to get a mortgage using maternity capital and how to do it

According to Decree of the Government of the Russian Federation No. 862, maternity capital, either fully or partially, can be used to improve housing conditions in the following ways:

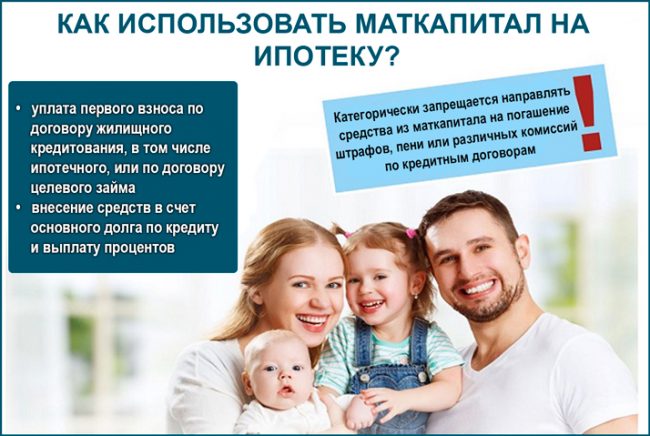

- To pay off the down payment when receiving a mortgage loan, to buy or build a house;

- To repay the debt and interest on it , including mortgage debt taken out for the purchase or construction of housing. Maternity capital cannot pay off fines, commissions or penalties for violations of the debt repayment schedule.

That is, maternity capital can be used to purchase housing, including to pay the down payment, to fully or partially repay the remaining balance of the mortgage loan.

Attention! Since 2009, government subsidies can be used to repay loans or interest on loans by the owner of maternity capital or a spouse. This can be done immediately after the birth of the child and receipt of the certificate, without waiting until the age of three.

According to the laws of the Russian Federation, certificates for maternity capital must be accepted by all financial institutions issuing loans, without exception. You can repay the balance of the loan or part of it at any time from the date of receipt. To pay part of the principal debt, a mortgage must be issued for the entire cost of the purchased home.

As mentioned earlier, maternity capital cannot be used to pay off penalties that were assessed for violations of the repayment schedule - late payments. Also, you cannot stop monthly accruals before the certificate is activated and the Pension Fund transfers the funds to the bank account. This will entail additional fines, penalties and increased interest.

The Pension Fund reserves the right to refuse to use maternity capital to repay a loan in the following cases:

- An incomplete package of documents was provided or incorrect information was provided;

- There were errors in the application for maternity capital;

- At the time of filing the application, the owner of the MK was deprived of parental rights or temporarily limited in them;

- The adoption of a child for whom maternity capital was issued was postponed or cancelled;

- The parent - the administrator of the certificate - failed in his duties and violated the rights of the child.

The refusal with a description of the reason is provided to the applicant only in writing. Those who do not agree with the decision of the Pension Fund can file a lawsuit to resolve the dispute.

Mortgage without down payment for maternity capital

Banks are much more loyal to borrowers who have the funds for a down payment. In this way, they are reinsured in case of a rapid drop in real estate prices, and also make sure that the potential borrower is able to competently manage finances to save at least 15-20% of the total cost of housing.

Even the Central Bank is suspicious of loans of this type and strongly does not recommend providing loans to citizens without any guarantees. Despite this, such programs are still in operation and are used by hundreds of thousands of people across the country. As a rule, they are valid for public sector employees or require higher interest rates to insure against risks.

Preferential lending programs are available for young families, military personnel, public sector workers and young parents, including for maternity capital. For such categories of citizens, subsidies are provided in the form of a loan or gratuitous payment.

In most cases, their size is not enough to fully pay for all housing, and citizens pay the remaining cost out of their own pockets. But in this case, maternity capital will be a good way to take out a home mortgage without a down payment. In such conditions, the state itself acts as a guarantor for the bank.

It is also useful to read: Is it possible to obtain maternity capital upon adoption?

Advantages and disadvantages of a mortgage using maternity capital

In Russia, the housing issue has always been acute. This is especially difficult for young families, whose capital is not yet enough to buy a home on their own. This is precisely what social programs of material support are designed for: the state helps Russians who have a child receive a number of benefits and financial privileges.

A mortgage under maternity capital is the same mortgage loan, only with the use of a certificate of maternity capital.

The certificate is issued by government agencies, but it cannot be cashed. The use of maternity capital is possible only for certain purposes: for example, in solving housing issues, obtaining education, medical treatment, etc. The diagram looks like this:

- The mother undergoes bureaucratic checks. After reviewing the documents, she is issued a certificate confirming her right to maternal capital;

- Next, the parent must use this certificate at his own discretion - for example, he can go through the popular “mortgage plus maternity capital” program;

- The bank receives a certificate from the borrower. The document is sent to government agencies. If everything is in order with the loan agreement and the certificate itself, the state transfers the money to the bank or any other organization where the parent applied;

- The lender receives money that is credited to the client as a down payment, partial early repayment, or other other transaction.

Accordingly, you cannot simply cash out maternity capital. In addition, the pragmatic use of the certificate is also complicated due to the high degree of bureaucratization in Russia. From here we can deduce the main disadvantages of a mortgage for maternity capital :

- Firstly, you will have to work hard to get the coveted 300-500 thousand rubles. Government authorities carefully check a citizen before he is issued a checkmate. capital;

- Secondly, not all banks agree to accept maternity capital as a down payment on a loan . The reason for this behavior is very simple: it is very difficult to receive money using a certificate due to the mass of paperwork. On average, it takes several months to cash out, and the bank does not always have that much time to wait for the money. Accordingly, banks, especially small ones, are very reluctant to accept certificates. It just so happens that housing with capital capital is issued only by large organizations cooperating with the state - Sberbank, VTB, Gazprombank, etc.;

- Banks often offer the client an alternative: the certificate will not be accepted as a down payment, but the bank agrees to consider it as a partial early repayment of the loan. In this way, you can reduce either the term of the loan agreement or the amount of the monthly payment. The downside is that young parents will need to find money for a down payment on their own, which is very difficult in the current economic situation;

- It should also be noted that it is almost impossible to buy an apartment with maternity capital without a mortgage. The amount received under the certificate ranges from 300-500 thousand rubles. This money is not enough to buy real estate. But maternity capital can be used to partially repay a loan or a down payment.

Of course, such a mortgage also has its advantages, otherwise there would not be such statistics: more than 70% of married couples who received maternity capital certificates used it to purchase housing on credit. The advantages are as follows:

- Standard, or even preferential interest rate. According to the legislation of the Russian Federation, banks are prohibited from increasing the rate only because the client wants to deposit a certain amount of the mortgage towards the certificate. Some banks, on the contrary, reduce the rate for clients with maternal capital in order to thus increase the company’s turnover;

- The realities in our country are such that attracting maternal capital is often the only possible way to acquire your own real estate. This is especially true for young couples;

- No matter how insignificant the amount of 300-500 thousand rubles may seem, this money is still an excellent help for newly formed cells of society.

If we briefly summarize the pros and cons of the proposal, we can say: yes, not everything is going smoothly with the certificate, and it is not a fact that it will be accepted by the bank. However, an additional 300-500 thousand rubles costs some running around government agencies and offices of a financial institution.

Matkapital as a down payment

Under preferential bank lending programs, maternity capital can act as a down payment. MK is issued to those families in which a second or more children were born or adopted, if the parents did not previously use maternity capital. As of January 1, 2020, according to the certificate, each family is entitled to 466,617 rubles.

A parent can spend the money received on a mortgage immediately after the birth of the child and receipt of the subsidy.

Then the whole process will look like this:

- The parent chooses a bank and a mortgage program that meets the conditions, which involves lending to improve housing conditions.

- There is no need to pay the first installment yourself, since the Pension Fund will transfer the required amount to the bank details.

- Next, the owner of the certificate submits an application for a mortgage at the bank.

- If the bank is ready to cooperate with the family, you can begin to search for a suitable developer or apartment on the secondary real estate market who are also ready to work in this mode.

- If the other party approves this procedure, the deal is concluded. All necessary documents are transferred to the Pension Fund of the Russian Federation, which transfers maternity capital to the bank.

Housing purchased under such conditions is registered as the common property of each family member (parents and each child).

Their shares are determined additionally by agreement. All family members, including minor children, must become home owners. If the child becomes an adult before the final repayment of the loan, he has the right to renounce his share in favor of his relatives.

Maternity capital as a down payment

- There are several nuances that need to be taken into account when using a mortgage loan certificate.

- The transfer of maternity capital from the Pension Fund of the Russian Federation takes from 2 months - if you have not yet submitted an application for funds, take this period into account. Moreover, it can take up to six months, so it is better to obtain a certificate in advance, and only then submit an application to the bank.

- When purchasing a home, all family members – both parents and children – should receive a share. Including minors.

- The down payment must be at least 10% of the cost of housing - just capital may not be enough. Taking into account the payments established in 2020, the maximum cost of housing that can be purchased using only maternity capital as a down payment is 4.5 million. When buying a more expensive apartment/house, you need to save up additional funds.

- It is better to choose ready-made housing - when receiving a loan to purchase an apartment in a building under construction, it is difficult to predict the completion date of construction. Unfortunately, some objects remain unfinished or are put into operation with serious delays. This is a high risk for the bank. And the approval rate for such applications is significantly lower.

- If the mortgage is issued for construction , calculate in advance a detailed estimate with deadlines for completing all work. The reason is similar to the previous point. It is important for the bank to understand at what point the collateral will be put into operation. This will significantly increase your chance of approval.

- Insurance is required – real estate insurance is mandatory when taking out a mortgage loan. This not only reduces the risk of failure, but also significantly reduces the interest rate. In addition, taking into account the duration of the loan, this also ensures security for the borrower himself.

Contrary to popular belief, insurance is not that expensive. And it is processed very quickly.

We advise you to look into the ratings of leading insurance companies to familiarize yourself with the nuances of the procedure and choose an insurer.

An example of calculating a mortgage payment if the down payment is capital

The largest and most reliable bank in Russia is Sberbank. And he also offers some of the most favorable lending conditions. With the help of maternity capital from Sberbank, you can cover the first mortgage payment in whole or in part.

For the calculation, you can take the most standard lending case with the following conditions:

- The intended purpose is to purchase an apartment on the primary real estate market, that is, in a new building;

- The loan will be issued in Moscow;

- The cost of the apartment is 3,000,000 rubles;

- The down payment to receive a lower interest rate will be 600,000 rubles;

- The loan will be issued for a period of 7 years.

Sberbank also has improved lending conditions if the certificate holder receives a salary on their card. Let's assume that it exists, and take into account that the family agreed to the terms of the Life Insurance program and reduced the final cost by another 1%.

You can also take the most positive option and assume that the parents rent an apartment from a developer who offers a discount for families participating in this program. Let's assume that this discount is 2.2%.

In this case, the bank can offer 2,400,000 Rubles as a loan at an interest rate of 6.5%. This means that every month the family must pay a minimum of 35,624 rubles, and its total monthly income cannot be less than 50,892 rubles.

Where to order a certificate for a mortgage

The procedure for obtaining such a document is quite simple, especially for those who have already encountered the preparation of similar papers. To understand where to get a certificate of maternity capital for a bank, you need to find out which department issued it.

- Contact your local Pension Fund (PFR) office in person or by mail.

- Use the official website or mobile application of the Pension Fund of Russia.

- Submit a request for a certificate through the Multifunctional Center (MFC).

- Or submit an appeal through the State Services portal.

Recommended article: How to calculate a mortgage with maternity capital using an online calculator

Any of the options will lead to results, but it is easiest to get a certificate from the Pension Fund about the balance of maternity capital if you do not have a state account. portal or website of the department.

How to obtain a certificate at the Pension Fund office

This method is the most popular. You just need to collect documents and visit the territorial department of the Pension Fund located in the applicant’s area of residence.

- Prepare papers confirming your right to receive a certificate of maternity capital balance.

- Make an appointment at your local FIU office and visit on the appointed day.

- Complete an application (its contents are stated in), submitting it along with the documentation, or send such papers by mail (then an appointment will not be required).

The date of acceptance of the application in accordance with is considered the date of its registration in the Pension Fund.

There is no need to pay for the certificate; it is issued free of charge. However, there are ways to obtain information that do not require personal presence.

How to obtain a document on the Pension Fund website or in the mobile application

Such options for issuing a certificate allow you to find out the balance of funds online (the right to remotely receive information about the amount is secured). But to obtain a housing loan, you will have to obtain documentary evidence of the availability of such money. You cannot simply submit information from a website or application to a bank.

How long a certificate of maternity capital balance is issued depends on the method of circulation. If the application is submitted online, it will take three days to prepare and send the response. The countdown starts from the moment the request is submitted. To submit an application for such a document, you need to:

- register on the State Services portal or on the official website of the Pension Fund;

- log in to the website or application of the Pension Fund;

- go to the section containing information about the mat. capital;

- select the point for issuing the certificate and the method of providing it (Russian Post);

- A registered letter is sent to the address specified in the application.

Recommended article: Stages of buying an apartment on the secondary market with a mortgage with maternity capital

Correspondence is sent within three days from the date of application, but it will arrive later. You also need to take into account the deadline for sending the letter, which you can find out at the Russian Post office. This is important, because the validity period of the certificate is also limited. Keep this in mind when submitting your application online.

How to order a certificate through the Multifunctional Center

In addition to the first two methods, you can request a certificate of the balance of maternity capital from the MFC. However, the period for receiving the document will increase significantly due to the circulation of the application through the authorities. The multifunctional center is an intermediary, and therefore it will forward the documents and application to the Pension Fund, and the department’s response will be sent to you. This will take up to 5 days.

The registration procedure is similar to applying through the Pension Fund:

- collect the necessary documents;

- fill out an application on site at the MFC;

- submit papers and appeal;

- wait for the answer and pick up the certificate.

If you have an account on the State Services portal, then it will be easier to issue a certificate for a mortgage that maternity capital has not been used.

How to get a certificate through the state website. services

First, you need to log in to the portal by logging into your personal account. If you don't have an account, you need to register one:

- Log in to the site by going to the new user registration section.

- Enter your information, contact information and a code that will be sent to your phone.

- Create a password and provide personal information (SNILS number, passport details, etc.).

- Confirm your identity by visiting a service center at the Post Office or MFC, through online banking, or by entering a code sent by registered mail.

Then you will be able to use the functionality of the portal by submitting documents online.

You can obtain a certificate of maternity capital balance through State Services as follows.

- Log in to your personal account, go to the All services section and find the item related to the Pension Fund (Pensions and benefits).

- Open the tab for informing citizens, then select the item for receiving services (Certificate of balance).

- Enter information about the applicant, indicate how to contact you, and submit the application for review.

The response will be a letter to the specified email address with a file in pdf format. Or the letter will be sent by regular mail. If the application is submitted online, there is no need to collect documentation. When visiting the MFC or Pension Fund in person, you will need to prepare a number of papers.

Is it possible to repay the remaining amount or part with a certificate?

If the family already has an existing housing loan, necessarily for the full amount of the property, the initial agreement is unlikely to indicate maternity capital.

Then the procedure will be as follows:

- The mortgaged apartment is issued to each family member, and the share participation agreement is registered with Rosreestr.

- After this, the Pension Fund transfers the loan funds to the account of the apartment seller towards the entire remaining amount or part thereof.

- If maternity capital pays off the entire balance, the family remains in settlement with the seller and the apartment becomes their complete disposal. Otherwise, until the loan is fully repaid and all interest for the use of funds is paid, the property will be pledged to the bank.

As for the bank, you need to interact with it according to the following scheme:

- From the bank that provided the mortgage loan, you need to get a certificate about the remaining amount of debt and declare your desire to pay it off with maternity capital.

- At the branch of the Pension Fund at the place of registration, the necessary documents are submitted, to which a loan certificate is attached.

- Within a month, the Pension Fund is studying the application for this method of disposing of the state subsidy. If the decision is positive, the Pension Fund transfers the money to the bank account within the next month.

If only part of the debt was repaid with maternity capital, after the transfer of funds, the bank approves a new schedule of monthly payments, which reduces their amount and the final payment terms.

It’s also useful to read: Is it possible to pay off a mortgage with maternity capital?

In the video there is additional information about repaying a mortgage using matkapital:

What documents are needed to obtain a certificate?

To receive such an extract, you will have to confirm your own rights to it. In order to preserve personal data, you need to confirm such rights even online (by entering personal information when filling out the form). If you apply in person, you will need the following documents for a certificate of maternity capital balance:

- identification card of the recipient of such state benefits;

- a certificate for each child and an application in the department form;

- certificate indicating the right to maternal capital.

Recommended article: How to sell a house bought with maternity capital

You must have your ID (passport) with you. You will need the original (). If copies are needed, they will be taken on the spot (as a rule, they are requested from the MFC). If the papers are sent online, the series and passport number, as well as the details of the remaining papers, will be sufficient.

Conditions of receipt

To receive a mortgage with partial payment by capital, the borrower must meet the following requirements:

- Have Russian citizenship and permanent residence in the region where the creditor bank is located;

- Have at least one year of total work experience;

- Work officially at your last place of work for at least 6 months;

- Be at least 21 years of age at the time of registration, and not older than 75 years at the time of full repayment.

The above requirements are common to all banks, but each financial organization has its own internal regulations and rules for approving loans.

They are rarely talked about and almost never listed in the public domain. For example, at Sovcombank, in most cases, loans are received by borrowers aged 35 years and older. Young couples are better off paying attention to other banks.

How to apply for a mortgage using capital in stages

In order to apply for a mortgage using maternity capital, you must:

- Collect 20% of the cost of the apartment. The rest of the amount is issued by the bank for the conclusion and payment of finished housing or shared construction on the primary real estate market.

- After that, the bank approves the issuance of the required amount, and then the family does the following: draws up and executes all documents for housing; registers the mortgage in Rosreestr to obtain an extract from the Unified State Register of Real Estate; The bank transfers all loan funds, along with the down payment, to the account of the home seller.

- Without waiting for the child to reach the age of three, the owner of the certificate obtains a certificate from the bank about the current debt, collects the entire package of documents for the Pension Fund and submits an application to dispose of the funds.

- In the event that the housing is not registered as shared ownership together with all family members, a notarial undertaking must be attached to the documents, which stipulates the mandatory allocation of shares to children and spouse no later than 6 months after repayment of the mortgage.

- The Pension Fund reviews applications and, if approved, transfers money to a bank account. On average, the entire procedure takes 1.5-2 months, during which the family is still obliged to pay the loan in full, without violating the payment schedule. Failure to pay may result in the Pension Fund’s application being rejected and fines being assessed.

Reference! You can also pay a down payment with maternity capital if the family does not have the opportunity to save 20% of the cost of housing. This option must be clarified with the creditor bank.